Most seniors don’t want to move to a nursing facility. Most families don’t want that either — at least not yet. In-home care is the practical middle ground: professional support that lets older adults stay in the home they know, surrounded by what’s familiar, while still getting the help they actually need.

The challenge is figuring out what type of care you need, what it costs in your area, and how to find providers you can actually trust. This guide walks through all of it.

Types of In-Home Care Services

Not all in-home care is the same. The right type depends on what your loved one actually needs — and those needs often change over time.

- Companion care — non-medical support focused on social interaction, conversation, errands, and light housekeeping. Best for seniors who are physically capable but isolated or at risk of cognitive decline from loneliness.

- Personal care / homemaker services — help with activities of daily living (ADLs): bathing, dressing, grooming, meal preparation, and mobility assistance. Provided by home health aides or personal care aides.

- Skilled home health care — medical care delivered at home by licensed nurses, physical therapists, occupational therapists, or speech therapists. Typically ordered by a physician after a hospitalization or for an ongoing medical condition.

- Memory care at home — specialized support for seniors with Alzheimer’s or other forms of dementia. Caregivers are trained in dementia communication, wandering prevention, and behavioral management.

- Hospice care at home — comfort-focused care for seniors with terminal illness who choose to spend their final months at home. Covers pain management, emotional support, and family counseling.

- Respite care — temporary in-home care to give family caregivers a break. Can be scheduled regularly or arranged for emergencies.

What In-Home Care Actually Costs in 2026

Costs vary significantly by location and type of care. Based on current national averages:

- Homemaker/companion services: $25–$35 per hour

- Home health aide services: $28–$38 per hour

- Skilled nursing visits: $150–$250 per visit

- Full-time (44 hrs/week) home health aide: $55,000–$75,000 per year

In high-cost states like California, New York, and Massachusetts, expect to pay 20–40% above these figures. In rural areas, expect lower rates but potentially fewer provider options.

💡 Cost tip: Most families underestimate how quickly costs add up. If your parent needs even 20 hours of care per week, you’re looking at $28,000–$40,000 annually. Build a clear financial picture before committing to any arrangement.

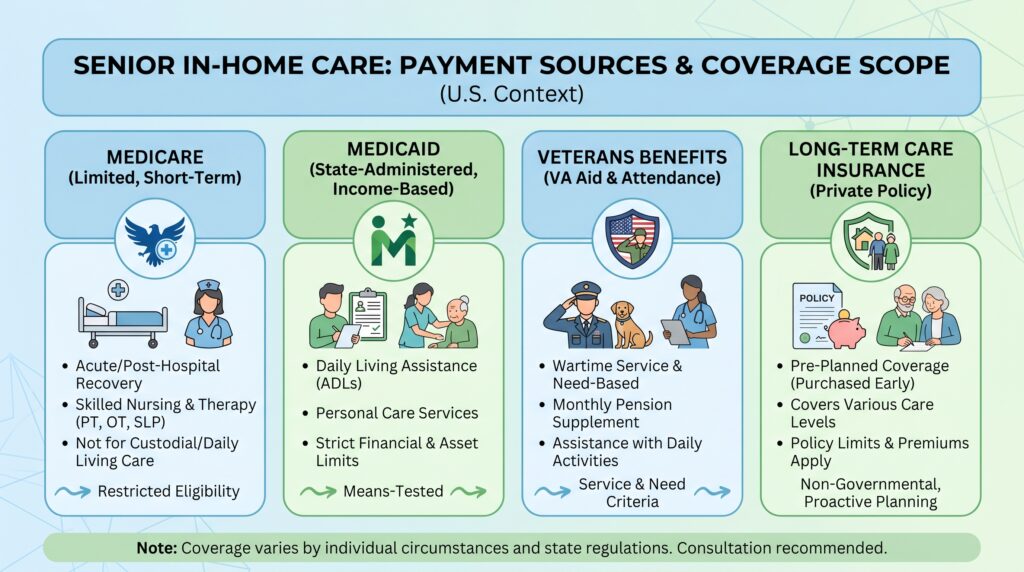

How to Pay for In-Home Care

Medicare

Medicare covers skilled home health services — nursing, therapy, wound care — when ordered by a doctor and provided by a Medicare-certified agency. It does not cover ongoing personal care or homemaker services when that’s the only care needed. The distinction matters, and many families are caught off guard by what Medicare won’t pay for.

Medicaid

Medicaid covers a broader range of in-home care services for eligible low-income seniors, including personal care and homemaker services in most states. Coverage and eligibility vary by state. The HCBS (Home and Community-Based Services) waivers allow states to offer alternatives to nursing home placement — look into your state’s specific waiver programs.

Long-Term Care Insurance

If your parent has an LTC policy, review the benefit triggers and elimination period carefully. Most policies require the senior to need help with at least two ADLs before benefits activate. Claims must be filed promptly — delays can forfeit coverage.

Veterans Benefits

The VA’s Aid and Attendance benefit provides financial assistance to veterans and surviving spouses who need help with daily activities. This benefit is significantly underutilized. If your loved one served in the military, check eligibility at va.gov — the monthly amounts can be substantial.

Private Pay

Most in-home care is paid out of pocket. Families often use a combination of the senior’s Social Security income, retirement savings, and family contributions. Start the conversation about finances early — waiting until a crisis limits your options.

How to Choose a Home Care Provider

The provider you choose will be in your loved one’s home, often alone with them. The stakes are high. Don’t shortcut this process.

- Agency vs. independent caregiver — agencies handle hiring, screening, training, backup coverage, and liability insurance. Independent caregivers cost less but shift all of that responsibility to you. For most families, a licensed agency is worth the premium.

- Check licensing and accreditation — verify the agency is licensed in your state. Look for accreditation from The Joint Commission or the Community Health Accreditation Partner (CHAP).

- Ask about caregiver screening — what background checks do they run? Are caregivers employees or contractors? What training do they receive? What happens if a caregiver calls out sick?

- Request references — speak directly with current or former clients. Online reviews are useful but not sufficient.

- Start with a trial period — begin with a few hours per week and evaluate how the caregiver interacts with your loved one. Chemistry matters as much as credentials.

- Get everything in writing — services provided, hours, rates, cancellation policy, and how disputes are handled. Verbal agreements become expensive misunderstandings.

Signs It’s Time to Consider In-Home Care

Most families wait too long. Watch for these indicators:

- Unexplained weight loss or signs of poor nutrition

- Missed medications or dangerous medication errors

- Recent falls or near-falls at home

- Declining personal hygiene that wasn’t previously an issue

- Increasing confusion, forgetfulness, or getting lost in familiar places

- Unpaid bills, financial disorganization, or signs of scam vulnerability

- Social withdrawal and increasing isolation

- Family caregiver showing signs of burnout — irritability, exhaustion, health neglect

If three or more of these apply, it’s time to have the conversation — not next month. Getting care in place before a crisis gives everyone more options and produces better outcomes.

Frequently Asked Questions

Q: Does Medicare pay for 24-hour in-home care?

No. Medicare covers part-time or intermittent skilled nursing or therapy services when medically necessary — it doesn’t cover round-the-clock personal care. For 24-hour care, you’ll need private pay, Medicaid (if eligible), or long-term care insurance.

Q: What’s the difference between a home health aide and a personal care aide?

Home health aides receive more formal training and can perform some clinical tasks — monitoring vital signs, assisting with medical equipment, wound care assistance — under supervision. Personal care aides provide non-medical support: bathing, dressing, grooming, meal prep.

Q: How do I find a reputable home care agency near me?

Start with Medicare’s Care Compare tool at medicare.gov, which lists Medicare-certified home health agencies and includes quality ratings. Your parent’s doctor or hospital discharge planner is also a strong referral source — they work with local agencies regularly and know which ones deliver consistent care.