Retirement should feel like relief—not uncertainty about medical bills. Yet for millions of American families, figuring out retiree health insurance becomes one of the most stressful financial transitions in later life.

A sudden change in coverage, rising premiums, and confusing Medicare choices can leave families scrambling for answers at the exact moment they want stability. The truth is, healthcare doesn’t get simpler when work coverage ends—it just shifts into a new system that requires careful planning.

This guide breaks everything down in plain language so you can understand your options, compare costs, and make confident decisions without feeling overwhelmed.

Types of Retiree Health Insurance Options

Retiree coverage in the U.S. isn’t one single plan—it’s a mix of systems that work together or separately depending on income, age, and employment history.

- Original Medicare (Part A & Part B)

The federal foundation of retiree health coverage. Part A covers hospital care, while Part B covers outpatient services like doctor visits. - Medicare Advantage (Part C)

Private insurance plans approved by Medicare that bundle hospital, medical, and often prescription coverage into one plan. - Medicare Supplement Insurance (Medigap)

Helps pay out-of-pocket costs like deductibles and copays that Original Medicare doesn’t fully cover. - Medicare Part D (Prescription Drug Plans)

Standalone plans that cover medications. - Employer-Sponsored Retiree Coverage

Some large employers continue offering group health insurance after retirement, often partially subsidized. - Medicaid (for low-income retirees)

Joint federal and state program that can significantly reduce or eliminate healthcare costs for eligible individuals. - Veterans Health Benefits

Coverage through the VA system for qualifying military veterans.

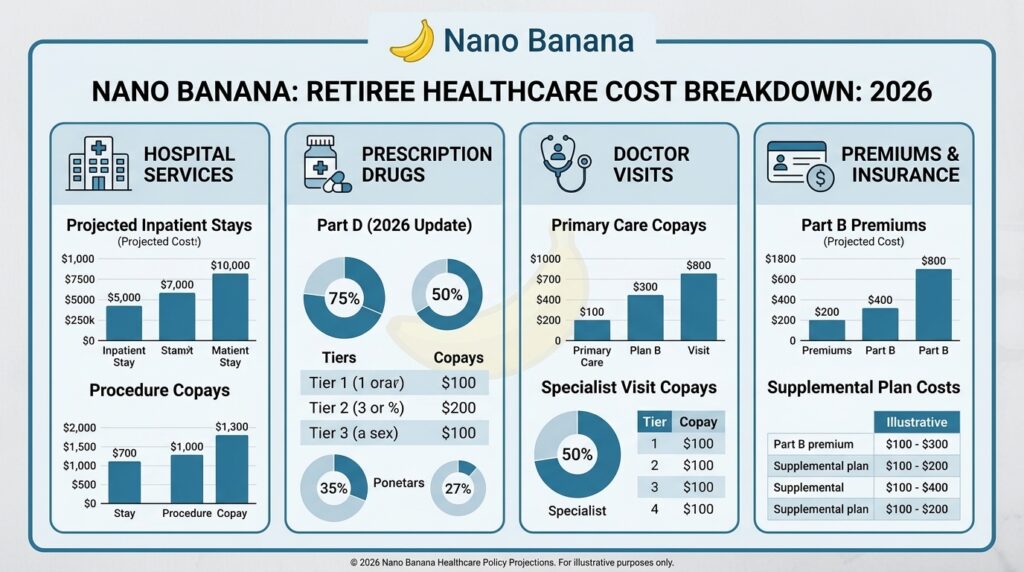

What Retiree Health Insurance Actually Costs in 2026

Costs in 2026 vary widely depending on income, location, and health status. Urban areas like California and New York generally see higher premiums than rural regions in the Midwest or South.

Typical monthly estimates:

- Medicare Part B premium: ~$185–$215/month (income-adjusted for higher earners)

- Medicare Advantage plans: $0–$90/month (many low-premium options, but higher copays)

- Medigap (Supplement plans): $120–$320/month depending on age and state

- Part D prescription coverage: $10–$60/month

Out-of-pocket costs like deductibles and copays can add another $2,000–$6,000+ annually, especially for chronic conditions.

💡 Note:

One of the biggest hidden costs in retiree health insurance is prescription drugs. Even with Medicare, medication expenses can exceed expectations unless you compare Part D or Advantage plans carefully each year during enrollment.

How to Pay for It / Financial Options

Paying for retiree healthcare often requires layering multiple resources. Families usually combine federal programs with private plans or supplemental coverage.

1. Medicare (Primary Coverage Base)

Most retirees enroll at age 65. It covers essential hospital and outpatient services but does not fully eliminate out-of-pocket costs.

2. Medicaid Assistance

For lower-income retirees, Medicaid can help cover premiums, copays, and long-term care expenses. Some individuals qualify for both Medicare and Medicaid (dual eligibility).

3. Veterans Benefits

Eligible veterans may access healthcare through VA facilities, significantly reducing private insurance reliance.

4. Employer Retiree Plans

Some employers continue offering coverage, which can act as a “wraparound” to Medicare.

5. Private Supplemental Insurance

Medigap or Medicare Advantage plans help reduce unpredictable medical bills, especially for chronic conditions.

6. Health Savings Accounts (HSAs)

While contributions stop after enrolling in Medicare, existing HSA funds can still be used tax-free for qualified medical expenses.

How to Choose a Provider / Make the Decision

Choosing retiree health insurance isn’t just about monthly premiums—it’s about predicting future healthcare needs.

Step-by-Step Decision Checklist:

- Confirm eligibility for Medicare and enrollment deadlines

- Compare total annual cost (not just monthly premiums)

- Review provider networks (especially specialists and hospitals)

- Check prescription drug coverage carefully

- Evaluate out-of-pocket maximums

- Look at travel coverage if you split time between states

- Review plan stability and yearly rate increases

- Ask for a “Summary of Benefits” before enrolling

Families often underestimate how much network restrictions matter until they need a specialist or hospital outside their plan’s coverage area.

Signs It’s Time to Consider Retiree Health Insurance Changes

Healthcare needs evolve quickly in retirement. It may be time to reassess coverage if:

- Medical visits are becoming more frequent or complex

- Prescription costs are rising each month

- You’re moving to a different state or region

- Your current plan network no longer includes key doctors

- You’re turning 65 and transitioning off employer coverage

- Out-of-pocket costs are becoming unpredictable

- A spouse has different coverage needs or eligibility

Stability in retirement healthcare isn’t about finding a “perfect” plan—it’s about adjusting coverage as life changes.

Frequently Asked Questions

Do retirees automatically get health insurance at 65?

No. Most people must actively enroll in Medicare during their Initial Enrollment Period. Missing deadlines can result in penalties or delayed coverage.

Is Medicare enough for most retirees?

Medicare covers a lot, but not everything. Many retirees add Medigap or Medicare Advantage to reduce copays, deductibles, and prescription costs.

What happens if I retire before age 65?

You’ll need temporary coverage through COBRA, a spouse’s plan, or the ACA Marketplace until Medicare eligibility begins.

Final Thoughts

Navigating retiree health insurance isn’t just a paperwork task—it’s a long-term financial strategy that directly affects comfort, security, and peace of mind in retirement.

The most successful families don’t just pick the cheapest plan; they choose coverage that balances predictable costs with access to the care their loved ones actually need.