For most American workers, Social Security taxes quietly come out of every paycheck—but few people fully understand where that money goes or how it shapes their future retirement income. Whether you’re supporting aging parents, planning your own retirement, or simply trying to make sense of your pay stub, these taxes directly affect your financial security later in life.

In 2026, rising wages, inflation adjustments, and evolving retirement expectations make it more important than ever to understand how Social Security taxes work—and what they mean for your long-term stability.

Types of Social Security Tax Contributions

Social Security taxes fall under the Federal Insurance Contributions Act (FICA). These contributions are divided based on how you earn income and your employment status.

- Employee Contributions (W-2 Workers)

Employees pay a fixed percentage of wages directly from each paycheck. - Employer Contributions

Employers match the employee’s contribution dollar-for-dollar. - Self-Employed Contributions (Self-Employment Tax)

Self-employed individuals pay both the employee and employer portions. - Tax on Social Security Benefits (Retirees)

Some retirees may pay federal income tax on benefits depending on total income. - Wage Cap Contributions

Only income up to a certain annual limit is subject to Social Security tax.

What Social Security Taxes Actually Cost in 2026

In 2026, Social Security taxes remain one of the most consistent payroll deductions in the United States.

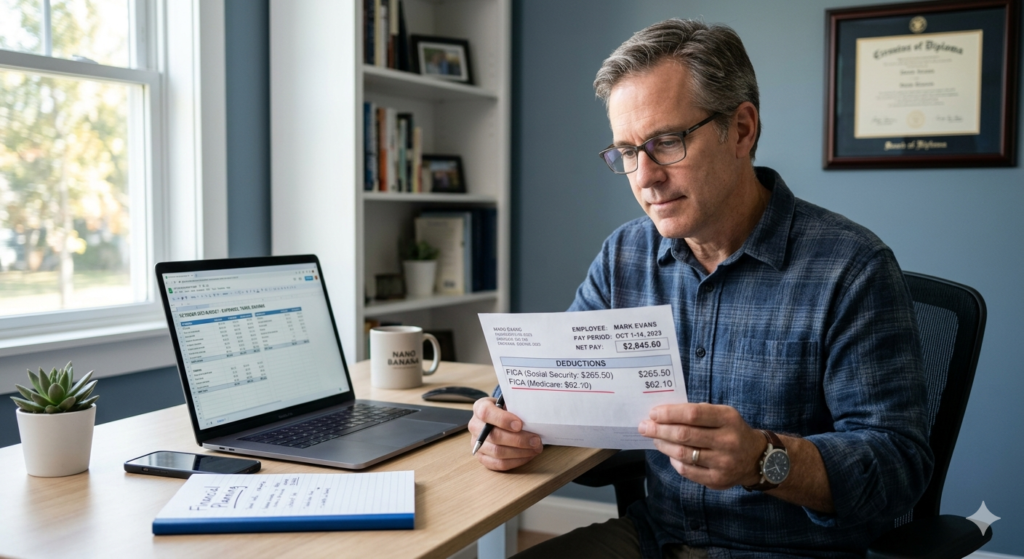

- Employee Rate: 6.2% of gross wages

- Employer Match: 6.2%

- Self-Employed Rate: 12.4% (combined share)

Wage Base Limit

Income is only taxed up to a yearly limit (commonly referred to as the “wage base cap”). In recent years, this cap has risen with inflation and is expected to remain in the mid-$170,000 range in 2026, though the exact figure is adjusted annually by the Social Security Administration.

Example

If you earn $80,000 annually:

- You pay approximately $4,960 in Social Security taxes per year

- Your employer matches the same amount

Regional Reality Check

While the tax rate is uniform nationwide, the impact feels different:

- Higher-income states like California and New York often see larger absolute deductions due to higher wages

- Rural areas may see smaller dollar contributions but similar percentage impact

💡 Tip/Note Box:

Even if Social Security taxes feel like “lost income,” they fund retirement, disability, and survivor benefits. Understanding your contribution helps you estimate future benefits more accurately—not just current deductions.

How to Pay or Adjust Social Security Taxes

Most people don’t manually “pay” Social Security taxes—they are automatically withheld. However, there are ways to manage how they affect your financial planning.

- W-4 Form Adjustments (Employees)

You can adjust withholding to better match your tax situation. - Estimated Tax Payments (Self-Employed)

Freelancers and contractors typically pay quarterly taxes directly to the IRS. - Voluntary Withholding for Retirees

If you receive Social Security benefits, you can request federal tax withholding using IRS Form W-4V. - Combining Income Streams Strategy

Retirement income from pensions, IRAs, or part-time work can affect how much of your benefits are taxed. - Tax Planning with a CPA or Advisor

Especially important if you are close to retirement or working while receiving benefits.

How to Plan Around Social Security Taxes

Understanding Social Security taxes isn’t just about payroll—it’s about long-term planning.

Step-by-Step Planning Checklist

- Review your annual earnings and W-2/1099 status

- Estimate future Social Security benefits using SSA tools

- Understand how working after retirement may affect taxes

- Evaluate combined household income (especially for couples)

- Coordinate withdrawals from retirement accounts strategically

The goal isn’t to avoid Social Security taxes—it’s to minimize surprises and maximize long-term benefits.

Signs It’s Time to Pay Closer Attention

You may need to take a closer look at Social Security taxes if:

- You’re earning near or above the annual wage cap

- You’re switching between W-2 and freelance work

- You’re approaching retirement age (62–70 range)

- You’re planning to claim benefits while still working

- You’ve recently had a major income change

- You’re supporting aging parents and planning shared retirement income

Frequently Asked Questions

Do I get Social Security taxes back if I don’t live long enough to use benefits?

No direct refund is issued. However, survivor benefits may be available to eligible family members based on your work history.

Why do high earners stop paying Social Security taxes mid-year?

Because income above the wage base limit is not taxed for Social Security purposes, though Medicare taxes may still apply.

Are Social Security taxes the same as income tax?

No. Social Security taxes are separate payroll taxes specifically funding retirement, disability, and survivor benefits—not general government spending.

Final Thoughts

Social Security taxes can feel like just another deduction, but they represent a long-term investment in retirement security. For many families, understanding how these taxes work is the difference between financial uncertainty and confident planning.

The key isn’t just knowing how much you pay today—it’s understanding how those contributions shape your stability decades from now.