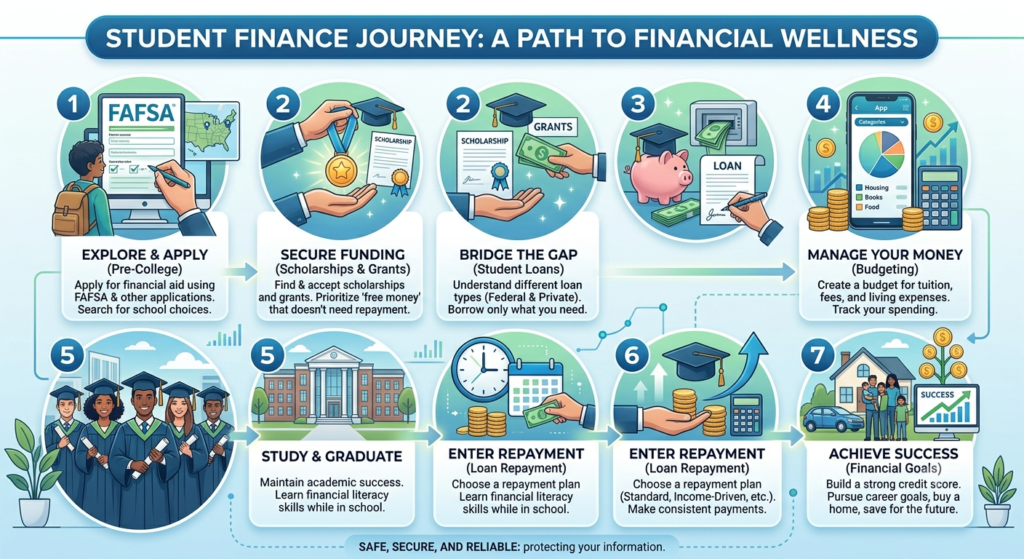

Paying for college is one of the biggest financial challenges students and families face. Understanding Student Finance can help you make informed decisions about tuition, housing, books, and everyday expenses while minimizing long-term debt.

Student finance includes a variety of funding options, such as federal student loans, private loans, grants, scholarships, work-study programs, and personal savings. Choosing the right combination can reduce borrowing costs and make higher education more affordable.

This guide explains the basics of student finance, available funding sources, budgeting tips, and strategies to manage your education costs in 2026.

What Is Student Finance?

Student Finance refers to the financial resources available to help students pay for higher education. These resources can cover tuition, housing, transportation, books, supplies, and other education-related expenses.

Financial aid may come from:

- Federal student loans

- Private student loans

- Grants

- Scholarships

- Work-study programs

- Savings and family contributions

The goal is to make education more accessible while helping students finance their studies responsibly.

Types of Student Financial Aid

Understanding the different types of aid can help you build a cost-effective funding plan.

Federal Student Loans

Federal student loans are often the first borrowing option because they typically offer fixed interest rates, flexible repayment plans, and borrower protections.

Common federal loan types include:

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Direct PLUS Loans

Scholarships

Scholarships provide financial assistance that usually does not need to be repaid. Awards may be based on academic achievement, athletics, leadership, community service, or financial need.

Grants

Grants are generally awarded based on financial need and typically do not require repayment if eligibility requirements are met.

Private Student Loans

Private loans are offered by banks, credit unions, and private lenders. Interest rates, repayment options, and eligibility requirements vary by lender.

Work-Study Programs

Federal Work-Study programs allow eligible students to earn money through part-time employment while attending school.

How to Apply for Student Finance

Applying early increases your chances of receiving available financial aid.

Follow these steps:

1. Complete the FAFSA

The Free Application for Federal Student Aid (FAFSA) is the starting point for most federal financial aid programs. Many colleges also use FAFSA information to determine institutional aid eligibility.

2. Apply for Scholarships

Search for scholarships offered by colleges, nonprofit organizations, employers, and community groups. Applying for multiple scholarships can significantly reduce education costs.

3. Review Your Financial Aid Offer

Compare grants, scholarships, loans, and work-study opportunities before accepting your aid package.

4. Borrow Responsibly

Only borrow what you reasonably need to cover educational expenses. Limiting debt today can reduce repayment challenges after graduation.

Managing Your Student Budget

Good financial habits can help reduce borrowing and improve long-term financial stability.

Consider these budgeting strategies:

- Track monthly income and expenses.

- Create a realistic spending plan.

- Build an emergency savings fund.

- Use student discounts whenever possible.

- Limit unnecessary credit card debt.

- Purchase used or digital textbooks when appropriate.

Learning to manage money while in school builds valuable financial skills for life after graduation.

Repaying Student Loans

Loan repayment usually begins after graduation, leaving school, or dropping below half-time enrollment, depending on the loan type.

Several repayment options may be available, including:

| Repayment Option | Best For |

|---|---|

| Standard Repayment | Borrowers seeking faster repayment |

| Graduated Repayment | Borrowers expecting income growth |

| Extended Repayment | Those needing lower monthly payments |

| Income-Driven Repayment | Borrowers with limited income |

Making on-time payments helps build a positive credit history and reduces the overall cost of borrowing.

Tips for Reducing College Costs

Paying less for college can reduce financial stress after graduation.

Helpful strategies include:

- Apply for financial aid as early as possible.

- Submit multiple scholarship applications.

- Attend community college before transferring, if appropriate.

- Buy used textbooks or rent course materials.

- Live within your budget.

- Review your financial aid package annually.

Small savings throughout your college years can significantly reduce the amount you need to borrow.

Frequently Asked Questions

What is student finance?

Student finance includes loans, grants, scholarships, work-study programs, and other financial resources that help students pay for college expenses.

Do I have to repay scholarships?

No. Scholarships generally do not require repayment as long as you continue to meet the award requirements.

What’s the difference between grants and loans?

Grants usually do not require repayment, while student loans must generally be repaid with interest according to the loan agreement.

Should I use private student loans?

Private loans may help cover remaining education costs after exhausting federal aid and scholarships. Compare interest rates, repayment terms, and borrower protections before borrowing.

How can I reduce student loan debt?

Apply for scholarships and grants, borrow only what you need, work part-time if possible, and follow a realistic budget throughout college.

Final Thoughts

Understanding Student Finance is essential for making informed decisions about paying for college while protecting your future financial well-being. By combining scholarships, grants, federal aid, responsible borrowing, and smart budgeting, you can reduce education costs and graduate with less debt.

Before accepting any financial aid package, compare all available funding options, estimate your future repayment obligations, and create a realistic education budget. A thoughtful approach to student finance can help you focus on your academic goals while building a stronger financial foundation for life after graduation.