Choosing the best insurance plans for seniors is an important step toward protecting both your health and your finances during retirement. Healthcare expenses often increase with age, making it essential to have coverage that fits your medical needs, prescription drug requirements, and budget.

Seniors today have several insurance options, including Original Medicare, Medicare Advantage, Medicare Supplement (Medigap), prescription drug plans, and long-term care insurance. Understanding how these plans work—and when they may be appropriate—can help you make informed decisions during enrollment.

This guide explains the most common insurance plans available to seniors, key features to compare, and practical tips for selecting the right coverage in 2026.

Why Seniors Need Health Insurance

Healthcare costs can become a significant part of retirement expenses. Insurance helps reduce the financial impact of doctor visits, hospital stays, prescription medications, and preventive care.

A comprehensive insurance plan may help cover:

- Primary care visits

- Specialist appointments

- Hospitalization

- Emergency medical services

- Prescription medications

- Preventive screenings

- Rehabilitation services

- Mental health care

Choosing the right coverage can improve access to quality healthcare while helping manage out-of-pocket expenses.

Types of Insurance Plans for Seniors

Several insurance options are available depending on your eligibility and healthcare needs.

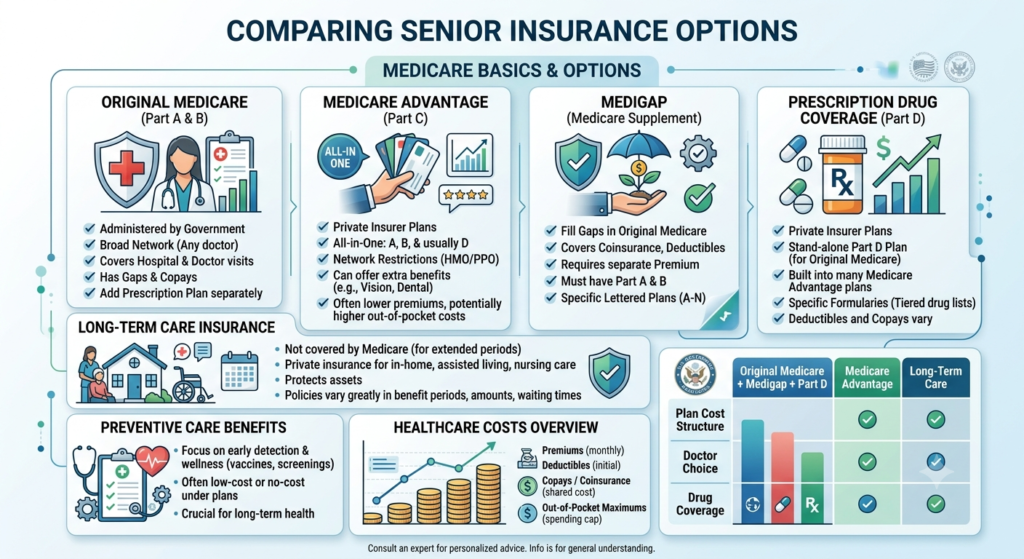

Original Medicare

Original Medicare includes Part A (hospital insurance) and Part B (medical insurance). It provides broad access to healthcare providers who accept Medicare but generally requires beneficiaries to pay deductibles, coinsurance, and certain out-of-pocket costs.

Medicare Advantage (Part C)

Medicare Advantage plans are offered by private insurance companies approved by Medicare. Many plans combine hospital, medical, and prescription drug coverage while offering additional benefits such as routine dental, vision, hearing, or wellness programs.

Medicare Supplement (Medigap)

Medigap policies help pay certain out-of-pocket costs not covered by Original Medicare, including copayments, coinsurance, and deductibles, depending on the plan selected.

Medicare Part D Prescription Drug Plans

Part D plans help cover the cost of prescription medications. Comparing formularies and participating pharmacies is important when selecting drug coverage.

Long-Term Care Insurance

Long-term care insurance may help pay for services such as assisted living, nursing home care, or in-home assistance that are generally not covered by Medicare.

How to Compare Insurance Plans

Comparing more than just monthly premiums can help you choose the right policy.

| Feature | Why It Matters |

|---|---|

| Monthly Premium | Your regular insurance cost |

| Deductible | Amount you pay before coverage begins |

| Out-of-Pocket Maximum | Limits annual healthcare expenses |

| Provider Network | Determines which doctors and hospitals are covered |

| Prescription Drug Coverage | Helps reduce medication costs |

| Additional Benefits | May include dental, vision, hearing, or fitness programs |

Reviewing these features carefully can help you balance affordability with comprehensive coverage.

Factors to Consider Before Enrolling

Every senior has different healthcare needs. Before selecting a plan, think about:

- Your current health conditions

- Prescription medications

- Preferred doctors and hospitals

- Expected medical procedures

- Travel habits

- Budget for premiums and out-of-pocket costs

Evaluating these factors can help you avoid paying for unnecessary coverage while ensuring your essential healthcare needs are met.

Tips for Choosing the Best Insurance Plan

Making an informed decision requires careful comparison.

Consider these recommendations:

- Compare multiple plan options during enrollment.

- Review provider networks before enrolling.

- Check prescription drug coverage for your medications.

- Estimate your annual healthcare expenses.

- Read the plan’s Summary of Benefits carefully.

- Review your coverage each year because benefits and costs may change.

Taking time to compare plans annually helps ensure your coverage continues to meet your healthcare needs.

Frequently Asked Questions

What is the best insurance plan for seniors?

There isn’t one plan that’s best for everyone. The ideal choice depends on your health, budget, preferred healthcare providers, and prescription medication needs.

Is Medicare enough by itself?

Original Medicare provides important coverage but doesn’t pay all healthcare expenses. Some beneficiaries choose additional coverage, such as Medigap or Medicare Advantage, to help manage out-of-pocket costs.

Do Medicare Advantage plans include prescription drug coverage?

Many Medicare Advantage plans include prescription drug coverage, but benefits vary by plan.

Is long-term care covered by Medicare?

Generally, Medicare does not cover most long-term custodial care. Individuals concerned about future long-term care needs may consider separate long-term care insurance.

Should I review my insurance every year?

Yes. Premiums, provider networks, covered medications, and plan benefits can change annually, making yearly comparisons worthwhile.

Final Thoughts

Choosing among the best insurance plans for seniors requires balancing healthcare needs, financial goals, and future medical expenses. Whether you’re considering Original Medicare, Medicare Advantage, Medigap, prescription drug coverage, or long-term care insurance, understanding each option can help you make a more confident decision.

Take time to compare plan costs, provider networks, covered services, and prescription benefits before enrolling. Reviewing your coverage each year ensures your insurance continues to support your health and retirement goals, providing greater peace of mind throughout 2026 and beyond.