Renting an apartment, condo, or house doesn’t mean you’re protected from unexpected financial losses. While your landlord’s insurance covers the building itself, it generally does not cover your personal belongings or liability. That’s where renters insurance becomes an essential part of your financial protection.

A renters insurance policy can help pay for damaged or stolen belongings, provide liability coverage if someone is injured in your rental home, and even cover temporary living expenses if your residence becomes uninhabitable after a covered event.

This guide explains how renters insurance works, what it covers, what it typically excludes, and how to choose the right policy for your needs in 2026.

What Is Renters Insurance?

Renters insurance is a type of property insurance designed for people who rent their homes. Unlike a homeowner’s insurance policy, it does not insure the building itself. Instead, it focuses on protecting your personal property and providing liability coverage.

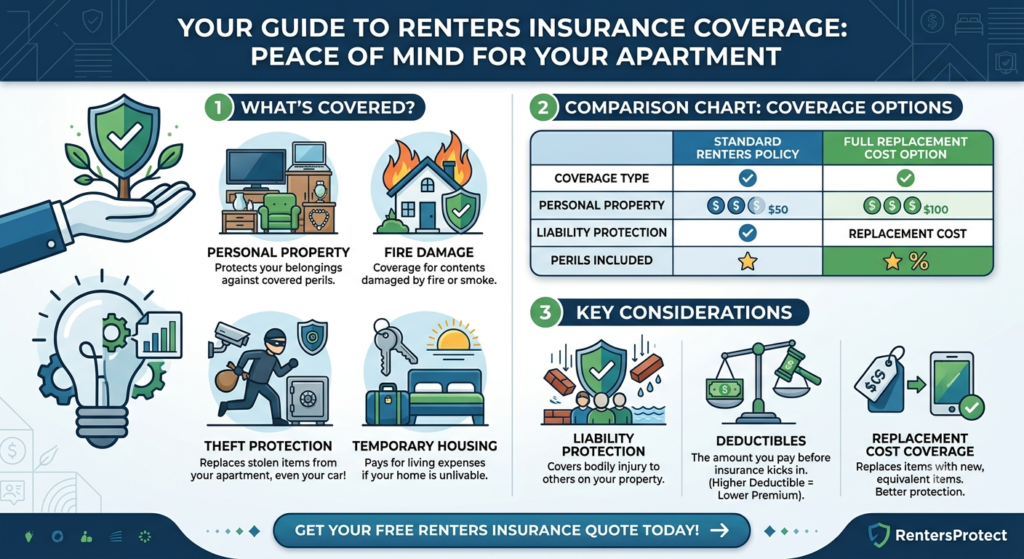

A standard renters insurance policy typically includes three main types of protection:

- Personal property coverage

- Personal liability coverage

- Additional living expenses (loss of use)

For many renters, this affordable coverage provides valuable financial protection against unexpected events.

What Does Renters Insurance Cover?

Coverage varies by insurer and policy, but most standard renters insurance plans include the following protections.

Personal Property

If your belongings are damaged or stolen due to a covered event such as fire, theft, vandalism, or certain weather-related incidents, your policy may help pay to repair or replace them.

Common covered items include:

- Furniture

- Clothing

- Electronics

- Kitchen appliances

- Jewelry (subject to policy limits)

- Bicycles

- Personal household items

Personal Liability

If someone is injured in your rental unit or you accidentally damage another person’s property, liability coverage may help pay legal expenses, settlements, or medical bills up to your policy limits.

Additional Living Expenses

If your rental home becomes temporarily uninhabitable because of a covered loss, renters insurance may help pay for:

- Hotel stays

- Restaurant meals

- Temporary housing

- Other eligible living expenses

This coverage can provide important financial relief during unexpected emergencies.

What Isn’t Covered?

Although renters insurance provides broad protection, it doesn’t cover every situation.

Common exclusions may include:

- Flood damage (separate flood insurance is usually required)

- Earthquake damage (unless additional coverage is purchased)

- Normal wear and tear

- Pest infestations

- Intentional damage

- High-value collectibles exceeding policy limits without endorsements

Reviewing your policy carefully helps you understand what protection is included and whether additional coverage is needed.

How to Choose the Right Renters Insurance Policy

Not all policies offer the same level of protection. Compare these important features before purchasing coverage.

| Feature | Why It Matters |

|---|---|

| Personal Property Limit | Determines maximum reimbursement for belongings |

| Liability Coverage | Protects against lawsuits and medical expenses |

| Deductible | Amount you pay before insurance coverage begins |

| Replacement Cost Coverage | Pays to replace items at today’s prices |

| Additional Living Expenses | Covers temporary housing after covered losses |

| Optional Endorsements | Adds protection for valuables and special items |

Choosing adequate coverage limits helps ensure you’re financially protected if an unexpected event occurs.

Tips to Save Money on Renters Insurance

Renters insurance is generally affordable, but these strategies can help lower your premium.

- Bundle renters and auto insurance with the same company.

- Install smoke detectors and security systems.

- Choose a higher deductible if appropriate.

- Maintain a good insurance history.

- Ask about available discounts.

- Create a home inventory with photos and receipts.

Keeping an updated inventory of your belongings can also simplify the claims process if you ever experience a loss.

Frequently Asked Questions

Is renters insurance required?

Renters insurance is generally not required by law, but many landlords require tenants to carry a policy as part of the lease agreement.

How much renters insurance do I need?

The amount depends on the value of your personal belongings and the level of liability protection you want. Creating a home inventory can help estimate appropriate coverage.

Does renters insurance cover theft outside my home?

Many policies provide limited protection for personal belongings stolen away from your residence, but coverage varies by insurer.

How much does renters insurance cost?

Premiums vary depending on your location, coverage limits, deductible, and insurer. Renters insurance is often one of the most affordable types of property insurance.

Does renters insurance cover roommates?

Generally, each roommate should have their own renters insurance policy unless the insurer specifically allows multiple unrelated individuals under one policy.

Final Thoughts

A renters insurance policy provides valuable protection for your personal belongings, financial security, and peace of mind. While your landlord’s insurance protects the building, it typically doesn’t cover your possessions or personal liability. That’s why having your own policy is an important part of responsible renting.

Before choosing a policy, compare coverage limits, deductibles, replacement cost options, and available discounts. Taking the time to understand your insurance needs today can help you recover more quickly from unexpected events tomorrow, giving you greater confidence and financial protection throughout 2026 and beyond.