If you’re paying high interest on an existing credit card, a balance transfer credit card may help you manage your debt more efficiently. These cards allow you to move an outstanding balance from one credit card to another, often with a lower introductory interest rate for a limited time.

A balance transfer doesn’t erase your debt—it simply transfers it to a new card. The main advantage is the opportunity to reduce interest charges, giving you more time to focus on paying down the principal balance instead of accumulating additional interest.

In this guide, you’ll learn how balance transfer credit cards work, who they are best suited for, their advantages and disadvantages, and how to choose the right one for your financial needs.

Quick Overview

A balance transfer credit card is commonly used to:

- Move debt from one credit card to another

- Reduce interest payments during a promotional period

- Simplify multiple credit card balances

- Pay off debt more efficiently

- Improve financial organization

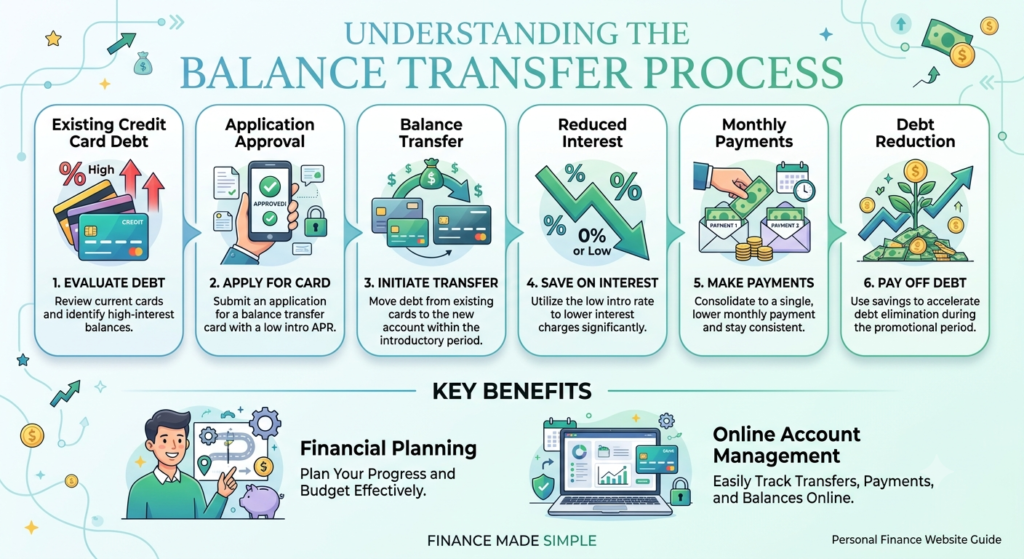

How Does a Balance Transfer Work?

The process is straightforward:

- Apply for a balance transfer credit card.

- Receive approval based on the issuer’s requirements.

- Request the transfer of your existing credit card balance.

- The new card issuer pays off the old balance.

- You make payments toward the balance on your new card.

Many balance transfer cards offer promotional interest rates for a limited period, allowing more of your payments to go toward reducing the amount you owe.

Is a Balance Transfer Card Right for You?

A balance transfer card may be a good option if you:

- Have high-interest credit card debt.

- Can make consistent monthly payments.

- Want to consolidate multiple balances.

- Plan to pay off the transferred balance before the promotional period ends.

- Are looking for a simpler repayment strategy.

It may be less suitable if you expect to continue adding significant new debt or cannot keep up with monthly payments.

Benefits of Balance Transfer Credit Cards

Lower Interest Costs

One of the biggest advantages is the opportunity to reduce interest payments during the introductory period.

Simplified Debt Management

Instead of keeping track of several payment due dates, you may only need to manage one monthly payment.

Faster Debt Repayment

When less money goes toward interest, more can be applied to reducing your outstanding balance.

Better Financial Organization

Combining balances into one account can make budgeting and tracking payments easier.

Online Account Management

Most issuers provide digital tools that allow you to:

- View balances

- Make payments

- Download statements

- Set payment reminders

- Monitor account activity

Things to Compare Before Applying

Not every balance transfer card offers the same benefits. Consider these factors before making a decision.

Introductory Interest Rate

Many cards provide a temporary promotional APR on transferred balances. Compare how long this promotional period lasts.

Balance Transfer Fee

Some issuers charge a balance transfer fee, usually calculated as a percentage of the transferred amount.

Regular APR

After the promotional period ends, the standard interest rate will apply to any remaining balance.

Credit Limit

Your approved credit limit determines how much debt you can transfer.

Transfer Time

Balance transfers may take several days or even a few weeks to complete, so continue making payments on your original account until the transfer is confirmed.

Tips for Paying Off Your Balance Faster

A balance transfer works best when paired with a solid repayment plan.

Helpful strategies include:

- Pay more than the minimum payment whenever possible.

- Create a monthly repayment budget.

- Avoid making new purchases on the transfer card.

- Set automatic payment reminders.

- Track your progress each month.

- Aim to repay the balance before the promotional rate expires.

These habits can help you reduce debt more quickly and avoid additional interest charges.

Common Mistakes to Avoid

Be aware of these common errors when using a balance transfer credit card.

- Missing payment due dates

- Ignoring balance transfer fees

- Continuing to accumulate new debt

- Paying only the minimum amount

- Forgetting when the promotional APR ends

- Closing old accounts without considering the impact on your credit history

Planning ahead can help you make the most of a balance transfer opportunity.

Frequently Asked Questions

What is a balance transfer credit card?

It’s a credit card that allows you to move debt from another credit card, often with a lower introductory interest rate for a limited period.

Does a balance transfer hurt my credit score?

Applying for a new card may result in a temporary hard inquiry, but responsible use and timely payments can support a healthy credit profile over time.

Can I transfer balances from multiple cards?

In many cases, yes. Whether you can transfer multiple balances depends on the issuer’s policies and your approved credit limit.

Is there a fee for transferring a balance?

Many balance transfer offers include a fee, although the amount varies by issuer and promotion.

Can I continue using my old credit card?

Yes, but if your goal is to reduce debt, it’s generally wise to avoid adding new balances until you’ve paid down your existing debt.

Final Thoughts

A balance transfer credit card can be an effective tool for reducing interest costs and simplifying debt repayment when used wisely. By comparing introductory offers, transfer fees, and repayment terms, you can choose a card that supports your financial goals.

The key to success is having a clear repayment strategy. Making consistent payments, avoiding new debt, and paying off your transferred balance before promotional rates end can help you save money and move closer to becoming debt-free.