A growing number of California educators are discovering that a pension alone may not provide the retirement lifestyle they imagined. Rising healthcare costs, longer life expectancies, and inflation have changed the retirement conversation. That is why interest in CalSTRS Pension vs 403(b) has surged among teachers at every stage of their careers.

For many educators, the question is no longer whether one plan is better than the other. Instead, it is how these two retirement tools work together to create long-term financial security.

Understanding the differences can help teachers make smarter decisions about retirement income, savings growth, and future financial flexibility.

Understanding the Basics: CalSTRS Pension vs 403(b)

At first glance, a pension and a retirement savings account may appear to serve the same purpose. In reality, they work very differently.

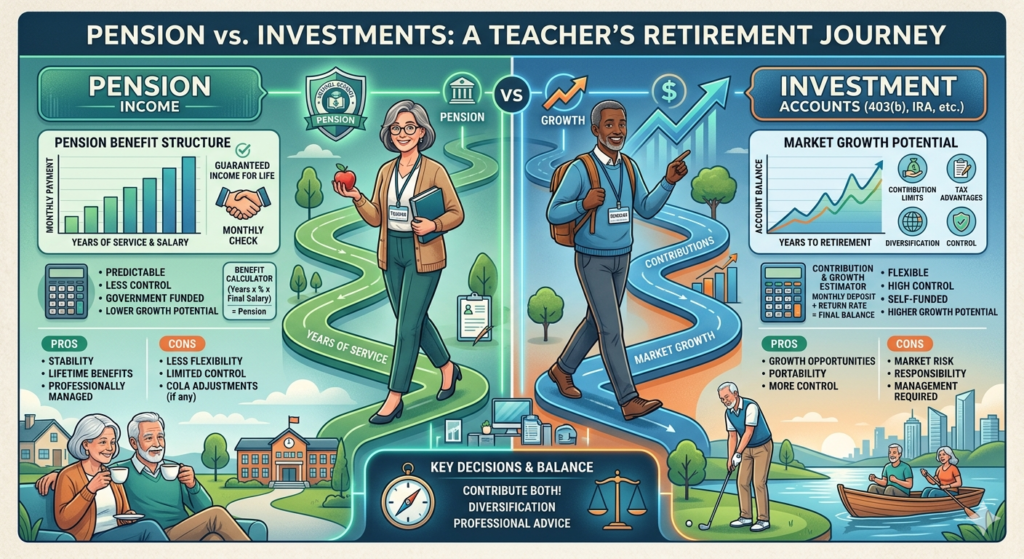

The CalSTRS pension is a defined-benefit plan. Your retirement income is calculated using a formula based on years of service, age at retirement, and final compensation. This structure provides predictable monthly payments throughout retirement.

A 403(b) retirement plan is a defined-contribution account. Contributions are invested, and the account’s value depends on investment performance over time. Unlike a pension, retirement income is not guaranteed.

This distinction makes the debate around Defined benefit vs defined contribution plan one of the most important decisions in California educator retirement planning.

Why Many Teachers Are No Longer Relying on a Pension Alone

A pension provides stability. However, stability does not always equal flexibility.

Many retired educators discover that their monthly pension income must cover expenses that continue to rise over time. Healthcare costs, housing expenses, and unexpected emergencies can place pressure on fixed retirement income.

A 403(b) can help bridge that gap by providing:

- Additional retirement savings

- Tax-advantaged growth

- Greater control over investments

- Supplemental retirement income

- Emergency financial flexibility

This is one reason financial planners increasingly encourage teachers to think beyond traditional Teacher pension California benefits.

Comparing CalSTRS and 403(b) Side by Side

CalSTRS Pension Advantages

The biggest advantage of CalSTRS retirement benefits is certainty.

Teachers know they will receive a predictable monthly payment for life after meeting eligibility requirements.

Benefits include:

- Guaranteed lifetime income

- No direct investment management required

- Protection from market volatility

- Survivor benefit options

- Strong retirement foundation

Potential limitations include:

- Limited flexibility

- Benefits tied to service years

- Inflation can reduce purchasing power over time

403(b) Advantages

A 403(b) retirement plan offers opportunities that pensions cannot.

Benefits include:

- Tax-deferred contributions

- Investment growth potential

- Flexible contribution amounts

- Ability to accumulate significant assets

- Additional retirement income source

Potential drawbacks include:

- Investment risk

- Market fluctuations

- No guaranteed payout

- Requires active planning

The tradeoff is clear: security versus flexibility.

The Most Effective Strategy May Be Using Both

Teachers often frame the discussion as an either-or decision.

In practice, many successful retirees use both.

The pension creates a reliable income floor. The 403(b) creates growth potential and financial flexibility.

Consider a mid-career teacher who expects a CalSTRS pension covering basic living expenses. By consistently contributing to a 403(b), that educator can create an additional pool of retirement assets for travel, healthcare costs, or major purchases.

This combination often produces stronger long-term Teacher retirement savings outcomes than relying on either option alone.

Common Mistakes Teachers Make

Retirement planning mistakes can be costly because they compound over decades.

Common errors include:

Assuming CalSTRS Will Cover Every Expense

Many educators overestimate how far pension income will stretch in retirement.

Waiting Too Long to Start a 403(b)

The power of compound growth favors early savers. Delaying contributions can significantly reduce future account balances.

Ignoring Investment Fees

Some 403(b) plans contain higher fees than teachers realize. Reviewing costs regularly can improve long-term returns.

Not Reviewing Beneficiary Information

Life changes such as marriage, divorce, or children often require updates to retirement account documents.

Frequently Overlooked Details About Teacher Retirement

One overlooked issue is longevity risk.

Retirees today often spend 20 to 30 years in retirement. A pension provides consistency, but additional savings can help maintain purchasing power over a lengthy retirement period.

Another overlooked factor is healthcare.

Many retirees underestimate future medical expenses. A supplemental savings account can provide valuable protection against unexpected costs.

Recent Trends Shaping California Teacher Retirement

Retirement planning has become more personalized.

Younger educators are paying closer attention to investment options and long-term wealth accumulation. At the same time, experienced teachers approaching retirement are increasingly evaluating how supplemental savings can improve retirement readiness.

Interest in CalSTRS vs 403(b) comparison searches has grown as educators seek more control over their financial futures.

Which Option Is Better?

Is a CalSTRS Pension or a 403(b) Better for Teachers?

Neither plan is universally better because they solve different retirement challenges.

A CalSTRS pension provides guaranteed lifetime income based on years of service and salary history. A 403(b) offers tax-advantaged savings and investment growth that can supplement pension benefits.

For many California educators, combining both creates a stronger retirement strategy by balancing income security with long-term growth potential.

The answer depends on career stage, savings goals, risk tolerance, and retirement expectations.

For most educators, the strongest retirement strategy combines the reliability of a pension with the flexibility of additional savings.

Retirement planning is rarely about choosing one winner. It is about building multiple sources of income that work together.

FAQ SECTION

Can teachers have both CalSTRS and a 403(b)?

Yes. Many California educators participate in CalSTRS while also contributing to a 403(b) plan.

Is CalSTRS enough for retirement?

It may provide a solid foundation, but many retirees benefit from additional savings to address inflation and healthcare costs.

What is the biggest advantage of a CalSTRS pension?

Guaranteed lifetime income based on a formula rather than investment performance.

What is the biggest advantage of a 403(b)?

Tax-advantaged savings and investment growth potential.

When should teachers start contributing to a 403(b)?

As early as possible to maximize compound growth over time.