Unexpected hospital stays can create financial stress even if you already have health insurance. Deductibles, copayments, transportation, childcare, and lost income can quickly add up. That’s where hospital indemnity insurance can help.

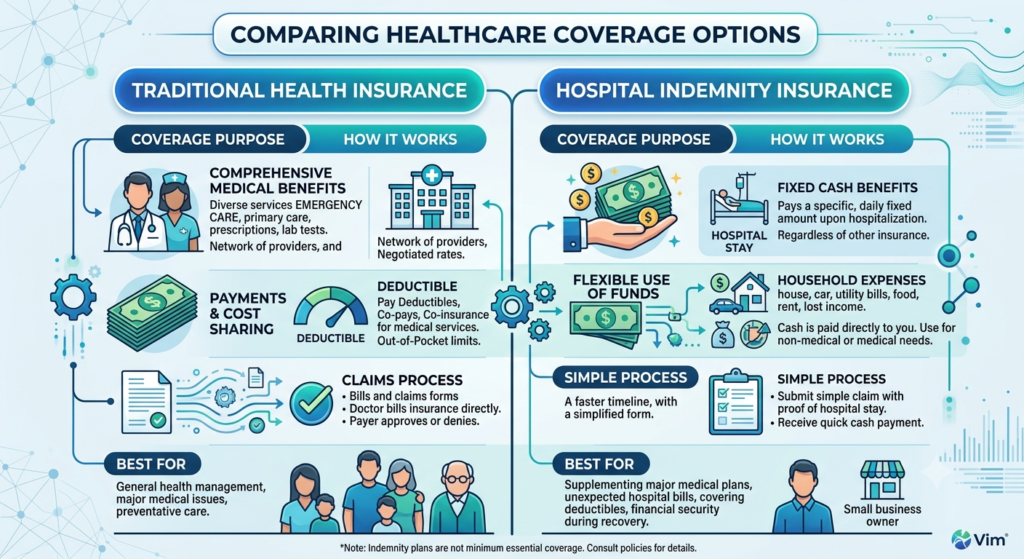

Hospital indemnity insurance is a type of supplemental health insurance that provides a cash benefit when you’re admitted to a hospital for a covered illness or injury. Unlike traditional health insurance, these payments are made directly to you—not your healthcare provider. You can use the money however you choose, whether it’s for medical bills, household expenses, or everyday living costs during recovery.

In this guide, you’ll learn how hospital indemnity insurance works, what it typically covers, its advantages and limitations, and how to decide if it’s the right addition to your healthcare coverage.

What Is Hospital Indemnity Insurance?

Hospital indemnity insurance is a supplemental insurance policy designed to help offset the out-of-pocket costs associated with a hospital stay.

Rather than paying healthcare providers directly, the insurer pays you a fixed cash benefit for covered hospital-related events, such as:

- Hospital admission

- Overnight stays

- Intensive care unit (ICU) stays

- Certain surgeries

- Emergency room visits (depending on the policy)

Because the benefit is paid directly to the policyholder, you have the flexibility to use the funds where they’re needed most.

How Does Hospital Indemnity Insurance Work?

After enrolling in a policy, you’ll pay a monthly premium. If you experience a covered hospitalization, you submit a claim with supporting medical documentation.

Once approved, the insurer provides a predetermined cash benefit based on your policy terms.

For example, a policy may include:

- Lump-sum hospital admission benefit

- Daily hospitalization benefit

- ICU benefit

- Surgical recovery benefit

The amount you receive depends on your specific plan rather than your actual medical expenses.

What Does Hospital Indemnity Insurance Typically Cover?

Coverage varies by insurer and policy, but many plans include benefits for common hospital-related expenses.

| Covered Benefit | Typical Purpose |

|---|---|

| Hospital admission | Initial cash payment after admission |

| Daily hospital stay | Fixed benefit for each covered day |

| ICU stay | Additional daily benefit |

| Outpatient surgery | Covered surgical procedures |

| Emergency services | Certain emergency treatments |

| Recovery assistance | Selected follow-up benefits |

Some policies also include optional riders for ambulance transportation, rehabilitation services, or wellness screenings.

Always review the policy details carefully to understand covered services, exclusions, waiting periods, and benefit limits.

Benefits of Hospital Indemnity Insurance

Many individuals choose hospital indemnity insurance because it provides financial flexibility during unexpected medical events.

Key benefits include:

- Helps cover deductibles and copayments

- Provides cash benefits paid directly to you

- Can assist with non-medical expenses such as rent, groceries, or childcare

- Complements existing health insurance

- Offers predictable benefit amounts for covered events

- May reduce financial stress during recovery

Since the benefit isn’t tied directly to medical bills, you decide how the money is spent.

Important Limitations to Consider

Hospital indemnity insurance is not intended to replace comprehensive health insurance.

Before purchasing a policy, understand that:

- Benefits are limited to covered events.

- Pre-existing condition exclusions may apply.

- Waiting periods may delay coverage for certain conditions.

- Policies have maximum benefit amounts.

- Routine medical care is generally not covered.

Reading the policy documents carefully helps prevent unexpected surprises when filing a claim.

Who Should Consider Hospital Indemnity Insurance?

Hospital indemnity insurance may be worth considering if you:

- Have a high-deductible health plan

- Want additional protection against unexpected hospital costs

- Have limited emergency savings

- Are concerned about out-of-pocket healthcare expenses

- Need supplemental coverage for family members

- Prefer additional financial flexibility during recovery

Employers sometimes offer hospital indemnity insurance as a voluntary workplace benefit, although individual policies are also available through private insurers.

Tips Before Buying a Policy

Before enrolling, compare several plans and consider:

- Monthly premium costs

- Hospital admission benefits

- Daily hospitalization payments

- Waiting periods

- Coverage exclusions

- Maximum annual benefit limits

- Renewal provisions

- Network requirements, if applicable

Choosing a policy that aligns with your health needs and budget can help maximize its value.

Frequently Asked Questions

Is hospital indemnity insurance the same as health insurance?

No. Hospital indemnity insurance is supplemental coverage that provides fixed cash benefits for covered hospital events. It does not replace comprehensive health insurance.

Can I use the benefit for non-medical expenses?

Yes. Cash benefits are generally paid directly to you and may be used for medical bills, transportation, childcare, mortgage payments, groceries, or other eligible expenses based on your needs.

Does every hospital stay qualify?

Not necessarily. Coverage depends on your policy’s terms, benefit schedule, exclusions, and waiting periods.

Is hospital indemnity insurance worth it?

It may be beneficial for individuals who face high out-of-pocket costs, have limited emergency savings, or want additional financial protection beyond their primary health insurance.

Can I have hospital indemnity insurance with employer health insurance?

Yes. Many people use hospital indemnity insurance alongside employer-sponsored health insurance to help cover deductibles and other uncovered expenses.

Final Thoughts

Hospital indemnity insurance can provide valuable financial support when unexpected hospital stays lead to expenses that traditional health insurance doesn’t fully cover. By paying fixed cash benefits directly to policyholders, it offers flexibility to handle both medical and everyday living costs during recovery.

Before purchasing coverage, compare policy benefits, exclusions, premiums, and waiting periods carefully. When paired with comprehensive health insurance, hospital indemnity insurance can serve as an additional layer of financial protection and provide greater peace of mind during medical emergencies.