Retirement feels like a long-awaited reward—until healthcare costs enter the conversation. For many American families, the emotional relief of leaving work is quickly replaced by a practical concern: How will we afford medical care for the next 20–30 years?

The truth is simple but often overlooked—retirement healthcare planning is just as important as saving for retirement itself. Medicare helps, but it doesn’t cover everything. And those gaps can quietly become one of the largest expenses in retirement.

This guide breaks down how retirement healthcare planning works in 2026, what it costs, how to prepare for coverage gaps, and how families can build a more financially stable healthcare strategy for the long term.

Types of Retirement Healthcare Planning

Retirement healthcare planning isn’t one single decision—it’s a combination of coverage layers that work together.

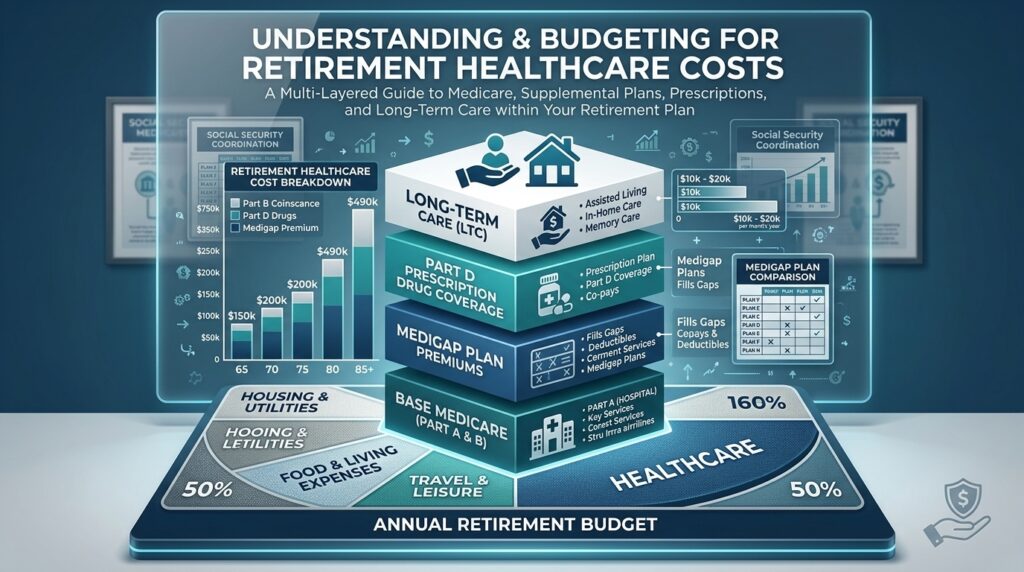

Core Healthcare Coverage Options

- Medicare (Primary Coverage for Seniors 65+)

Includes Part A (hospital), Part B (medical), and optional Part D (prescriptions). - Medicare Advantage Plans (Part C)

Bundled plans that combine Medicare benefits with additional services like vision and dental. - Medigap (Supplemental Insurance)

Helps cover deductibles, copays, and coinsurance not paid by Original Medicare. - Employer Retiree Health Plans

Some retirees continue receiving partial or full healthcare coverage through former employers. - Medicaid (Income-Based Coverage)

Provides healthcare support for low-income seniors or those with high medical expenses. - Long-Term Care Insurance

Covers services like assisted living, nursing homes, or in-home care support.

Each layer plays a role in reducing out-of-pocket healthcare costs during retirement.

What Retirement Healthcare Actually Costs in 2026

Even with Medicare, healthcare remains one of the largest retirement expenses.

Estimated Annual Healthcare Costs (2026)

| Category | Cost Range |

|---|---|

| Medicare Part B Premiums | $2,000–$3,000/year |

| Medicare Advantage Premiums | $0–$2,000/year |

| Medigap Plans | $1,500–$3,500/year |

| Prescription Drugs | $500–$6,000/year |

| Out-of-Pocket Care | $2,000–$10,000/year |

Total Estimated Annual Spending

- Low medical needs: $4,000–$7,000/year

- Moderate needs: $7,000–$15,000/year

- High medical needs: $15,000–$30,000+/year

Regional Differences Matter

Healthcare costs vary significantly:

- Higher costs in California, New York, Florida metro areas

- Lower costs in rural Midwest and smaller Southern states

- Urban hospitals often mean higher copays and facility fees

[💡 Tip/Note Box]

Medicare reduces risk—but it does not eliminate cost. Many retirees underestimate out-of-pocket spending, especially for prescriptions and specialist care.

How to Pay for Retirement Healthcare

Paying for healthcare in retirement requires combining multiple funding sources.

Medicare (Foundation Coverage)

Most retirees rely on Medicare as the base layer of coverage after age 65.

- Hospital coverage (Part A)

- Doctor visits (Part B)

- Prescription drugs (Part D optional)

Supplemental Insurance

Many retirees purchase additional coverage:

- Medigap to reduce out-of-pocket costs

- Medicare Advantage for bundled services

Medicaid Support

For qualifying low-income seniors:

- Covers long-term care in some cases

- Helps reduce premiums and medical expenses

Health Savings Accounts (HSAs)

If available before retirement:

- Tax-free contributions

- Tax-free withdrawals for medical expenses

- Powerful long-term healthcare funding tool

Personal Savings

Retirees often rely on:

- Retirement accounts (IRA, 401(k), 403(b))

- Emergency savings

- Pension income

How to Choose a Retirement Healthcare Strategy

The best healthcare plan depends on health status, budget, and risk tolerance.

Step 1: Evaluate Current Health Needs

Ask:

- Do I take regular prescriptions?

- Do I see specialists frequently?

- Do I expect chronic condition care?

Step 2: Compare Medicare Options

Choose between:

- Original Medicare + Medigap

- Medicare Advantage plans

Step 3: Review Provider Networks

Check:

- Doctor availability

- Hospital access

- Specialist coverage

Step 4: Calculate Total Annual Cost

Include:

- Premiums

- Deductibles

- Copays

- Prescription costs

Step 5: Plan for Long-Term Care

Many families forget this step:

- Assisted living

- Home health care

- Nursing facilities

Signs Your Retirement Healthcare Plan Needs Attention

Healthcare needs change quickly in retirement.

Watch for these warning signs:

- Your prescription costs are increasing year over year

- You don’t understand your Medicare coverage gaps

- You haven’t reviewed plans during open enrollment

- You are unsure what long-term care would cost you

- Your doctors are no longer in-network

- You rely on a single coverage source without backup

- Your health conditions have changed significantly

Early adjustments can prevent major financial stress later.

Frequently Asked Questions

Does Medicare cover all retirement healthcare costs?

No. Medicare covers many essential services but does not fully cover prescriptions, dental, vision, long-term care, or all out-of-pocket expenses.

When should I start retirement healthcare planning?

Ideally 5–10 years before retirement, but it’s still valuable to plan at any stage. Earlier planning increases flexibility and lowers long-term costs.

Is Medicare Advantage better than Medigap?

Neither is universally better. Medicare Advantage is often lower cost upfront, while Medigap provides more predictable out-of-pocket expenses. The right choice depends on health needs and budget.

Final Thoughts

Retirement healthcare planning is one of the most important—and often underestimated—parts of retirement readiness. While Medicare provides a foundation, it is only the beginning of the financial picture.

The real key is preparation: understanding coverage gaps, estimating real costs, and building a plan that accounts for changing health needs over time.

Families who plan early tend to experience fewer financial surprises and more confidence in retirement. It’s not about predicting every medical need—it’s about building enough flexibility to handle them when they arrive.

A strong healthcare plan doesn’t just protect your finances—it protects your peace of mind throughout retirement.