A better credit score can save you thousands of dollars over your lifetime. It can help you qualify for lower mortgage rates, better auto loan terms, higher credit limits, and even improve your chances of renting an apartment. If you’ve been wondering how to check your credit report and raise your score, you’re already taking one of the smartest steps toward improving your financial future.

The good news is that improving your credit doesn’t happen through shortcuts—it happens through consistent habits and informed decisions. By reviewing your credit report regularly, correcting mistakes, and managing your accounts responsibly, you can gradually build a stronger credit profile.

Whether you’re preparing to buy a home, finance a vehicle, or simply gain more financial confidence, this guide will walk you through everything you need to know in 2026.

Why Your Credit Report Matters

Your credit report is a detailed record of how you’ve managed credit over time. Lenders, landlords, insurance companies, and sometimes employers may review portions of your credit history when making decisions.

A typical credit report includes:

- Personal Information – Name, addresses, and identifying details.

- Credit Accounts – Credit cards, mortgages, student loans, and auto loans.

- Payment History – Records of on-time and late payments.

- Credit Inquiries – Companies that have recently reviewed your credit.

- Public Records – Certain financial records, when applicable.

Your credit score is calculated using information from your credit report. If the report contains inaccurate information, your score may be lower than it should be.

That’s why experts recommend reviewing your credit report regularly—not just when applying for a loan.

How to Check Your Credit Report for Free

Many consumers assume checking their credit report costs money, but that’s not always the case.

You can access your credit report from the nationwide credit reporting agencies through authorized services. Reviewing your own report creates a soft inquiry, which does not lower your credit score.

When reviewing your report, pay close attention to:

- Incorrect personal information

- Accounts you don’t recognize

- Late payments reported by mistake

- Duplicate accounts

- Incorrect balances

- Accounts that should have been removed

- Signs of identity theft

If you discover an error, file a dispute as soon as possible with the credit reporting agency and provide supporting documentation.

💡 Tip/Note Box

Review your credit report at least once every few months—even if you aren’t planning to borrow money. Catching an error early can prevent bigger financial problems and may help improve your credit score over time.

Proven Ways to Raise Your Credit Score

Improving your credit score doesn’t happen overnight, but these strategies consistently make the biggest difference.

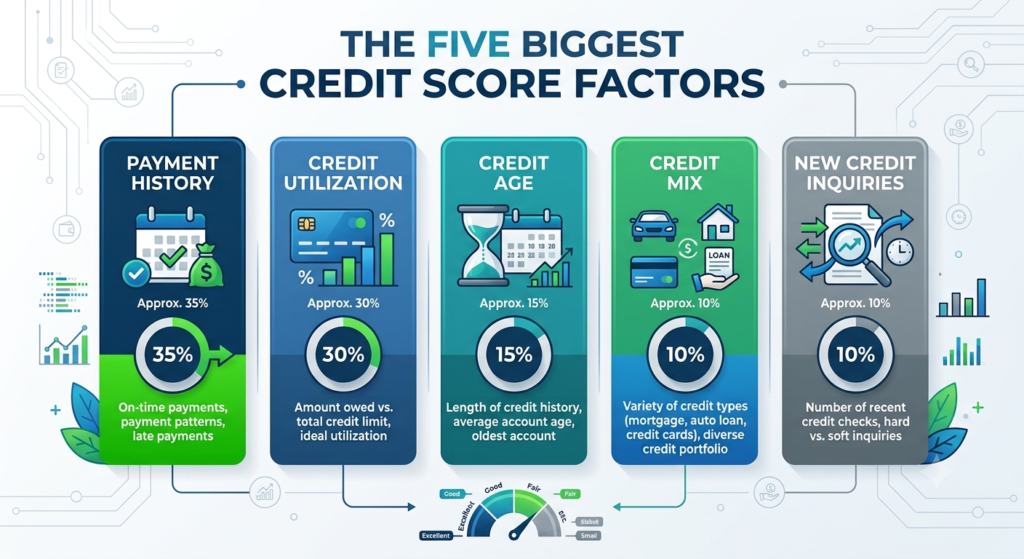

1. Pay Every Bill on Time

Payment history is one of the most influential factors in most credit scoring models.

Set up:

- Automatic payments

- Payment reminders

- Calendar alerts

Even one missed payment can remain on your credit report for years.

2. Lower Your Credit Utilization

Credit utilization measures how much of your available revolving credit you’re using.

For example:

- Credit Limit: $10,000

- Balance: $2,000

- Utilization: 20%

Many financial experts recommend keeping utilization below 30%, while staying under 10% may provide even stronger results for some consumers.

3. Avoid Applying for Too Much New Credit

Every application for new credit can generate a hard inquiry.

Several hard inquiries within a short period may temporarily reduce your score, especially if you’re applying for multiple credit cards.

Apply only when you genuinely need new credit.

4. Keep Older Accounts Open

The age of your credit history matters.

Closing an older credit card account may reduce your available credit and shorten your average account age, both of which can affect your score.

If there’s no annual fee, keeping older accounts open can often be beneficial.

5. Diversify Your Credit Mix

A healthy mix of credit accounts may strengthen your credit profile over time.

Examples include:

- Credit cards

- Auto loans

- Student loans

- Mortgages

- Personal loans

However, never borrow money solely to improve your credit mix.

Common Credit Report Mistakes to Watch For

Errors on credit reports are more common than many people realize.

Watch carefully for:

Incorrect Late Payments

Sometimes payments are reported late even though they were made on time.

Accounts That Don’t Belong to You

Unknown accounts could indicate reporting errors or identity theft.

Incorrect Credit Limits

An incorrect limit can artificially increase your utilization ratio.

Duplicate Debt Listings

The same account should not appear multiple times.

Outdated Information

Certain negative items should no longer appear after the applicable reporting period.

Correcting these mistakes won’t always increase your score immediately, but it helps ensure lenders see an accurate picture of your financial history.

When to Monitor Your Credit More Frequently

Checking your credit once a year is a good starting point, but certain situations call for closer monitoring.

Consider reviewing your credit report more often if:

- You’re preparing to buy a home.

- You’re shopping for an auto loan.

- You’re applying for a new credit card.

- You’ve recently paid off significant debt.

- You were denied credit unexpectedly.

- You’ve experienced identity theft or a data breach.

- You notice suspicious account activity.

Regular monitoring can help you respond quickly to inaccuracies or fraudulent activity.

Frequently Asked Questions

Does checking my own credit report lower my credit score?

No. Reviewing your own credit report is considered a soft inquiry and does not affect your credit score.

How long does it take to improve a credit score?

Minor improvements may appear within a few months after reducing balances or correcting errors. Larger improvements often require consistent responsible credit management over a longer period.

What’s more important: my credit report or my credit score?

Both matter. Your credit report contains the information used to calculate your credit score. Keeping your report accurate is one of the best ways to support a healthier score.

Final Thoughts

Learning how to check your credit report and raise your score is one of the most valuable financial skills you can develop. Your credit report tells the story of your borrowing history, while your credit score helps lenders assess your financial reliability.

By reviewing your report regularly, disputing inaccuracies, paying bills on time, maintaining low credit utilization, and avoiding unnecessary debt, you can steadily improve your credit profile. Progress may not happen overnight, but every positive financial habit moves you closer to better borrowing opportunities, lower interest rates, and greater financial security.

The strongest credit scores are built through consistency—not quick fixes. Start by checking your credit report today, make informed improvements, and let those small steps create lasting financial confidence throughout 2026 and beyond.