Paying for college often requires more than scholarships and savings. Understanding the available student loan options can help you finance your education while minimizing long-term debt. The right loan depends on your financial needs, interest rates, repayment flexibility, and future career plans.

Students today can choose from federal student loans, private student loans, parent loans, and refinancing options after graduation. Each option has different eligibility requirements, repayment terms, and borrower protections. Knowing the differences before borrowing can save thousands of dollars over the life of your loan.

This guide explains the most common student loan options, compares their features, and offers practical advice for borrowing responsibly in 2026.

What Are Student Loan Options?

Student loan options are financing programs that help students and, in some cases, parents pay for college-related expenses such as tuition, housing, books, meal plans, and transportation.

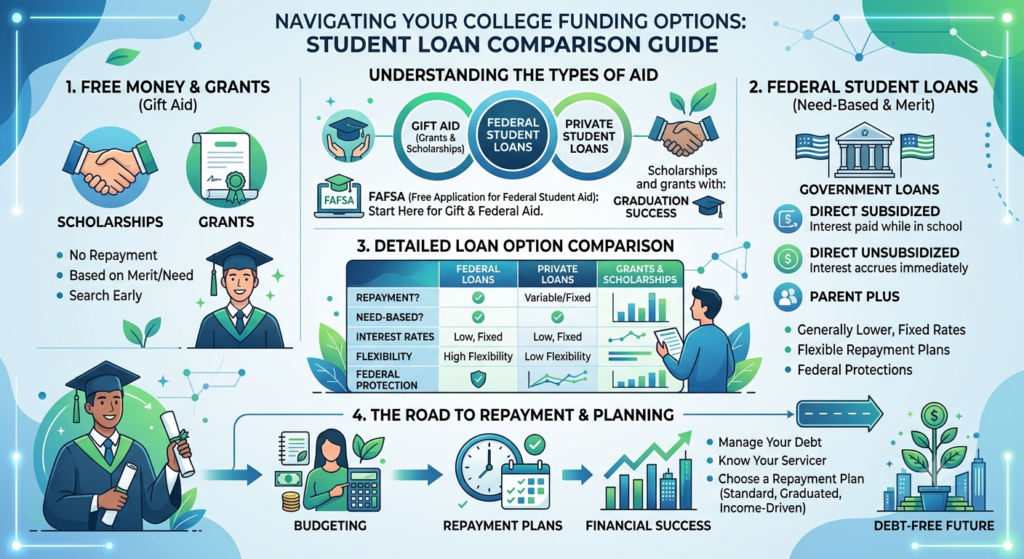

The most common sources of student loans include:

- Federal student loans

- Private student loans

- Parent loans

- Student loan refinancing (after graduation)

Because every borrower’s financial situation is different, it’s important to compare loan terms carefully before accepting any offer.

Types of Student Loans

Understanding the available loan types helps you make informed borrowing decisions.

Direct Subsidized Loans

These federal loans are available to eligible undergraduate students with demonstrated financial need. The government pays the interest while you’re enrolled at least half-time and during certain other qualifying periods.

Direct Unsubsidized Loans

Available to undergraduate and graduate students, these loans do not require financial need. Interest begins accruing as soon as the loan is disbursed.

Direct PLUS Loans

Graduate students and eligible parents of dependent undergraduate students may qualify for PLUS Loans to help cover education expenses not paid by other financial aid.

Private Student Loans

Private lenders—including banks, credit unions, and online financial institutions—offer student loans that may help bridge funding gaps after federal aid has been exhausted. Approval often depends on credit history, income, or a qualified co-signer.

Federal vs. Private Student Loans

Many financial experts recommend exploring federal loans before considering private lenders because of their borrower protections.

| Feature | Federal Student Loans | Private Student Loans |

|---|---|---|

| Credit Check | Usually not required for most student borrowers | Often required |

| Interest Rates | Fixed rates established annually | Fixed or variable rates depending on lender |

| Income-Driven Repayment | Available for eligible borrowers | Usually not available |

| Loan Forgiveness Programs | Available for qualifying borrowers | Rarely offered |

| Deferment and Forbearance | Federal protections available | Varies by lender |

Comparing these differences can help you choose the financing option that best supports your long-term financial goals.

How to Choose the Right Student Loan

Before borrowing, evaluate more than just the interest rate.

Consider these factors:

Total Borrowing Cost

Estimate how much you’ll repay over the life of the loan, including interest and fees.

Monthly Payments

Choose repayment terms that fit your expected budget after graduation.

Repayment Flexibility

Federal loans generally provide more flexible repayment options, including income-driven repayment plans for eligible borrowers.

Future Career Plans

Students entering lower-paying professions may benefit from repayment programs designed to make monthly payments more manageable.

Tips for Borrowing Responsibly

Borrowing wisely today can reduce financial stress after graduation.

Follow these best practices:

- Complete the FAFSA before considering private loans.

- Accept grants and scholarships before borrowing.

- Borrow only what you truly need.

- Track your total student loan balance each year.

- Understand repayment obligations before signing.

- Consider paying accrued interest while in school if possible.

Responsible borrowing helps keep future monthly payments manageable.

Frequently Asked Questions

What are the main student loan options?

The primary options include Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans, and private student loans offered by financial institutions.

Should I choose federal or private student loans?

Many students begin with federal loans because they often provide fixed interest rates, flexible repayment plans, and borrower protections. Private loans may be helpful if additional funding is needed after federal aid has been exhausted.

Can I refinance my student loans?

Yes. Some borrowers refinance after graduation to obtain a lower interest rate or simplify repayment. Refinancing federal loans into private loans may result in the loss of certain federal benefits.

How much should I borrow?

Borrow only the amount necessary to cover qualified education expenses after accounting for scholarships, grants, savings, and other financial aid.

Do I have to start repaying immediately?

Repayment timelines depend on the type of loan. Many federal student loans provide a grace period after leaving school or graduating before repayment begins.

Final Thoughts

Understanding your student loan options is essential for financing your education without creating unnecessary long-term debt. Federal loans, private loans, and parent borrowing programs each offer unique benefits and considerations, making it important to compare eligibility requirements, repayment terms, and total borrowing costs.

Before accepting any loan, review your financial aid package carefully, maximize scholarships and grants, and borrow only what you need. A thoughtful borrowing strategy can help you complete your education while maintaining greater financial flexibility and confidence well beyond graduation in 2026.