Choosing between different checking and savings account options is one of the first steps toward building a healthy financial future. Whether you’re opening your first bank account, switching financial institutions, or looking for higher interest rates, understanding the available options can help you make smarter decisions.

Checking accounts are designed for everyday spending, while savings accounts help you set money aside for future goals. Many banks and credit unions also offer account packages that combine both, making it easier to manage your finances from one place.

This guide explains the most common checking and savings account options, their benefits, and how to choose the best combination for your needs in 2026.

What Is a Checking Account?

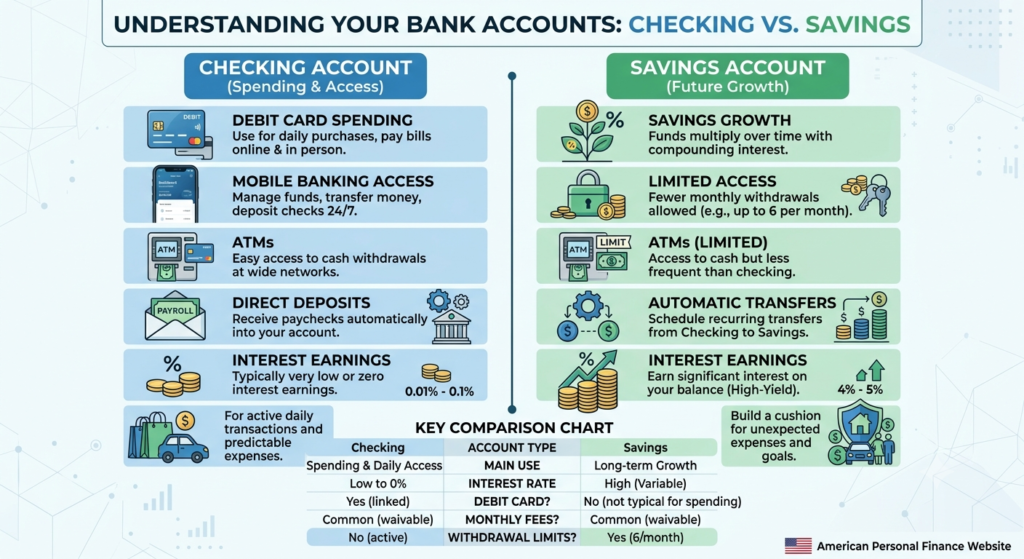

A checking account is built for daily financial transactions. It allows you to deposit money, pay bills, write checks, use a debit card, and receive direct deposits from your employer.

Common features include:

- Debit card access

- Online and mobile banking

- Bill pay services

- ATM withdrawals

- Direct deposit

- Mobile check deposits

Many checking accounts offer little or no interest, but they provide easy access to your money whenever you need it.

What Is a Savings Account?

A savings account is intended for money you don’t plan to spend regularly. These accounts generally earn interest, helping your balance grow over time while keeping your funds accessible for emergencies or future expenses.

Savings accounts are commonly used for:

- Emergency funds

- Vacation savings

- Home down payment

- Holiday expenses

- Education costs

- Major purchases

Many online banks offer higher annual percentage yields (APYs) than traditional brick-and-mortar banks.

Common Checking and Savings Account Options

Different financial institutions offer accounts tailored to various needs.

Standard Checking Account

Ideal for everyday banking, these accounts usually include debit card access, online banking, and direct deposit support.

Interest Checking Account

Some checking accounts pay interest on your balance while still providing daily transaction capabilities. They may require higher minimum balances.

Student Checking Account

Designed for young adults and college students, these accounts often have reduced fees and simplified account requirements.

High-Yield Savings Account

High-yield savings accounts typically offer significantly higher APYs than traditional savings accounts, making them attractive for long-term savings goals.

Money Market Account

Money market accounts combine features of checking and savings accounts by offering interest earnings along with limited check-writing or debit card access.

Joint Accounts

Joint checking or savings accounts allow two or more people, such as spouses or family members, to manage shared finances together

Comparing Checking and Savings Account Features

When evaluating checking and savings account options, compare more than just interest rates.

| Feature | Checking Account | Savings Account |

|---|---|---|

| Everyday spending | ✔ | Limited |

| Debit card | ✔ | Sometimes |

| Earns interest | Sometimes | Usually |

| Bill payments | ✔ | Limited |

| ATM access | ✔ | Limited |

| Best for | Daily expenses | Saving money |

Looking at the complete package helps you choose an account that matches your financial habits.

How to Choose the Right Account

The best account depends on your personal financial goals.

Consider these factors:

- Monthly maintenance fees

- Minimum balance requirements

- Interest rates (APY)

- ATM network availability

- Mobile banking features

- Customer service quality

- FDIC or NCUA insurance

- Overdraft protection options

If you primarily bank online, an online-only institution may offer lower fees and higher savings rates. If you prefer in-person assistance, a traditional bank with local branches may be a better fit.

Tips for Managing Both Accounts

Using checking and savings accounts together can simplify money management.

Helpful strategies include:

- Deposit your paycheck into checking.

- Automatically transfer part of each paycheck to savings.

- Keep emergency funds separate from spending money.

- Review account statements regularly.

- Enable account alerts for low balances and large transactions.

- Avoid unnecessary overdraft fees by monitoring your checking balance.

Automating transfers helps you save consistently without requiring extra effort each month.

Frequently Asked Questions

Should I have both a checking and savings account?

Yes. A checking account is ideal for daily spending, while a savings account helps you build financial security and earn interest on money you don’t need immediately.

Are online banks safe?

Most online banks are insured by the FDIC, while credit unions are typically insured by the NCUA. Always verify insurance coverage before opening an account.

What is a high-yield savings account?

A high-yield savings account offers a higher APY than many traditional savings accounts, allowing your savings to grow faster over time.

Can I open multiple savings accounts?

Yes. Many people maintain separate savings accounts for emergency funds, vacations, home purchases, or other financial goals.

Do checking accounts earn interest?

Some do. Interest checking accounts pay interest, although rates are generally lower than those offered by high-yield savings accounts.

Final Thoughts

Exploring different checking and savings account options allows you to choose banking products that fit your lifestyle and financial goals. A checking account supports everyday spending and bill payments, while a savings account helps grow your money through interest and encourages disciplined saving.

Before opening an account, compare fees, interest rates, digital banking tools, ATM access, and customer support. Selecting the right combination of accounts can make managing your finances easier and help you build a stronger financial foundation in 2026.