Your credit score is more than just a number—it can influence whether you’re approved for a mortgage, auto loan, credit card, apartment rental, or even certain job opportunities. If you’ve ever searched “check my credit score”, you’re already taking an important step toward understanding your financial health.

The good news is that checking your own credit score is simple, usually free, and does not lower your score. Knowing where you stand helps you spot errors, detect identity theft, and make smarter borrowing decisions. This guide explains the safest ways to check your credit score, what it costs, how to interpret it, and when it’s time to take action.

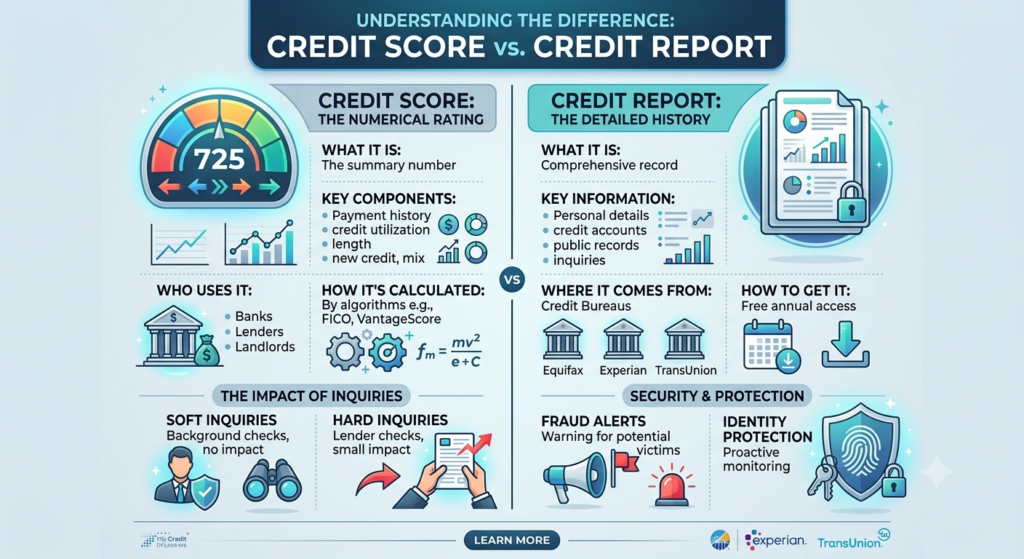

Types of Credit Scores and Credit Reports

Not all credit scores are the same. Understanding the different types can help you know what lenders may see.

- FICO® Score

- The most widely used credit score by lenders.

- Scores typically range from 300 to 850.

- Commonly used for mortgages, auto loans, and credit cards.

- VantageScore®

- Developed by the three major credit bureaus.

- Also ranges from 300 to 850.

- Frequently used by banks and free credit monitoring services.

- Credit Reports

- Detailed records of your credit history.

- Include payment history, credit accounts, balances, inquiries, and public records.

- Available from the three nationwide credit bureaus.

- Bank or Credit Card Credit Scores

- Many financial institutions provide free credit score access to customers.

- Scores may update monthly.

- Credit Monitoring Services

- Notify you about significant changes to your credit profile, such as new accounts or hard inquiries.

What Checking Your Credit Score Actually Costs in 2026

One of the biggest misconceptions is that you must pay to see your credit score.

In reality, many trusted sources allow you to check your credit score for free.

| Service | Typical Cost |

|---|---|

| Credit Score Through Many Banks | Free |

| Credit Card Issuer Credit Score | Free (if offered) |

| Credit Monitoring Services | Free to Premium Plans |

| Credit Reports | Free from authorized sources under applicable federal provisions |

Premium monitoring plans may range from $10–$40 per month, depending on features such as identity theft monitoring, dark web surveillance, and multi-bureau credit tracking.

Unlike some financial products, checking your credit score costs the same regardless of where you live. Whether you’re in California, New York, Texas, or a rural community, free options are widely available online.

💡 Tip/Note Box

Checking your own credit score creates a “soft inquiry,” which does not affect your credit score. Only certain lender-initiated “hard inquiries” may have a temporary impact when you apply for new credit.

Where to Check Your Credit Score for Free

There are several safe and reliable ways to monitor your credit.

Through Your Bank or Credit Card Issuer

Many banks and credit card companies now provide free credit score updates as part of your online account.

Free Credit Monitoring Services

Several reputable financial websites offer free credit score access along with educational tools and score tracking.

Official Credit Reports

Reviewing your credit report helps verify that the information used to calculate your score is accurate. Look for:

- Incorrect account balances

- Unknown credit accounts

- Missed payments reported in error

- Identity theft indicators

Identity Protection Services

Some monitoring services combine credit score tracking with fraud alerts, identity restoration support, and account monitoring.

How to Choose a Trusted Credit Monitoring Service

Not every credit monitoring platform offers the same features.

Use this checklist before signing up.

✔ Understand Which Score Is Provided

Some services provide a VantageScore®, while many lenders rely on FICO® Scores. Knowing which score you’re viewing helps set expectations.

✔ Compare Monitoring Features

Look for:

- Credit score updates

- Fraud alerts

- Identity theft monitoring

- Multi-bureau tracking

- Credit report access

✔ Review Privacy Policies

Choose companies with strong security practices and transparent privacy policies.

✔ Avoid Unnecessary Paid Plans

If your needs are basic, free monitoring from your bank or card issuer may be enough.

✔ Check Update Frequency

Some services refresh scores weekly, while others update monthly.

Signs It’s Time to Check Your Credit Score

Monitoring your credit regularly can help you catch problems before they become expensive.

You should check your credit score if:

- You’re planning to apply for a mortgage or auto loan.

- You’re applying for a new credit card.

- You’ve paid down significant debt.

- You’ve recently been denied credit.

- You suspect identity theft.

- You haven’t reviewed your credit in over a year.

Regular monitoring helps you understand how financial decisions affect your credit over time.

Frequently Asked Questions

Does checking my own credit score lower it?

No. When you check your own credit score, it results in a soft inquiry that does not impact your credit score.

How often should I check my credit score?

For most consumers, checking your score once a month is a good habit. More frequent monitoring may be helpful if you’re preparing for a major loan or watching for identity theft.

Why is my credit score different on different websites?

Different services may use different scoring models, such as FICO® or VantageScore®, and may receive updated information at different times. Small variations are common.

Final Thoughts

Searching “check my credit score” is one of the smartest financial habits you can develop. Regularly reviewing your credit score and credit report helps you identify errors, monitor your progress, and prepare for major financial milestones like buying a home or financing a vehicle.

The best part is that checking your own score is generally free, secure, and does not hurt your credit. By using trusted providers, reviewing your reports for accuracy, and practicing responsible credit habits—such as paying bills on time and keeping balances low—you can strengthen your financial future and make informed borrowing decisions with confidence.