For many educators, retirement doesn’t feel like a distant milestone—it feels like a financial puzzle that slowly reveals itself over time. After years of teaching, supporting students, and building a career, teachers often discover that retirement planning is less about a single pension check and more about how multiple benefits work together.

The challenge is that teacher retirement benefits include pensions, healthcare coverage, tax-advantaged savings plans, and sometimes Social Security—all of which interact in ways that are not always obvious until retirement is close.

This guide breaks down teacher retirement benefits in 2026, what they cost, how they work together, and how educators can build a more stable and confident retirement plan.

Types of Teacher Retirement Benefits

Teacher retirement benefits are typically built from several interconnected systems rather than a single source of income.

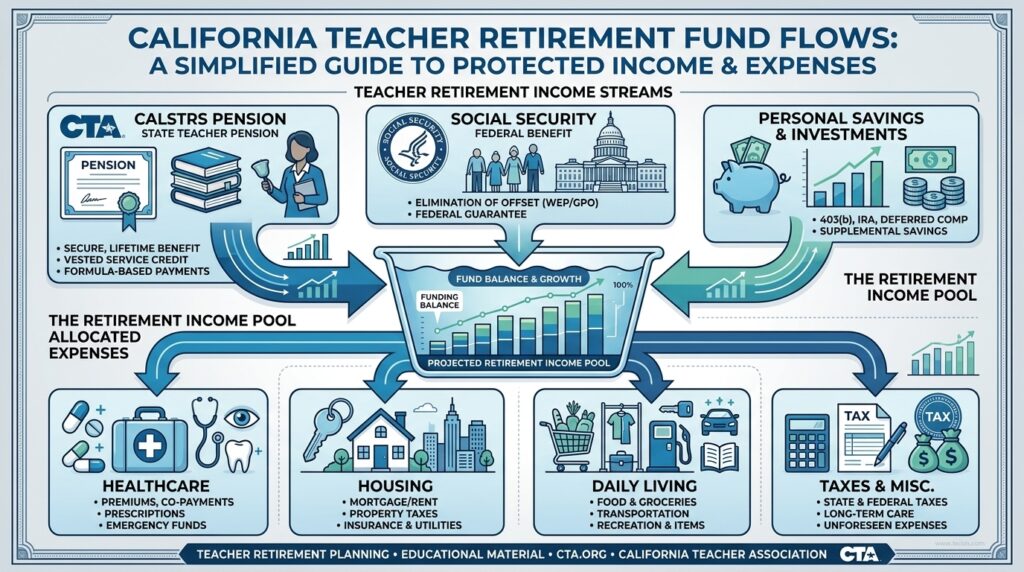

Core Benefit Categories

- Defined Benefit Pension (CalSTRS or Similar Systems)Provides guaranteed monthly income based on salary history, years of service, and retirement age. This is the foundation of most teacher retirements.

- 403(b) Retirement Savings PlansTax-advantaged accounts that allow teachers to supplement pension income through voluntary contributions.

- 457(b) Deferred Compensation PlansOffers additional tax-deferred savings with flexible withdrawal options after separation from service.

- Social Security (for eligible teachers)Applies to educators who have worked in Social Security-covered employment outside teaching or in certain districts.

- Retiree Healthcare BenefitsEmployer-supported medical coverage that may continue after retirement depending on district rules and service years.

- Disability and Survivor BenefitsProvides financial protection in case of disability or death, supporting families during unexpected life events.

- Personal Savings and InvestmentsIncludes IRAs, brokerage accounts, and emergency funds that provide flexibility beyond structured retirement systems.

What Teacher Retirement Benefits Actually Cost in 2026

Teacher retirement benefits are not purchased in a traditional sense, but they involve long-term payroll contributions and future healthcare expenses that shape retirement readiness.

Typical Payroll Contributions During Career

| Benefit Type | Estimated Contribution |

|---|---|

| CalSTRS Pension | ~8%–11% of salary |

| Social Security (if applicable) | 6.2% of wages |

| Medicare Tax | 1.45% of wages |

| 403(b)/457(b) Savings | Voluntary (0%–15%+) |

Estimated Retirement Income (2026)

- Teacher Pension Income: $2,200–$6,800+ monthly depending on service years

- Social Security (if eligible): $1,200–$3,800+ monthly

- Supplemental Savings: Highly variable depending on contributions

Healthcare Cost Reality

Even with retiree coverage, healthcare remains one of the largest expenses:

- $300–$900/month in premiums (varies widely)

- $5,000–$15,000/year in out-of-pocket costs

- Higher costs in California, New York, and other high-cost states

[💡 Tip/Note Box]

A strong pension does not eliminate healthcare risk. Many retirees find that medical expenses rise faster than pension adjustments over time, making supplemental savings essential.

How Teachers Fund Their Retirement Income

Teacher retirement benefits come from multiple coordinated sources that work together in retirement.

Step 1: Pension Contributions During Employment

Teachers contribute a percentage of their salary to pension systems like CalSTRS throughout their careers.

Step 2: Supplemental Retirement Accounts

Teachers voluntarily build additional savings through:

- 403(b) plans

- 457(b) deferred compensation plans

- IRAs and Roth IRAs

Step 3: Employer-Supported Benefits

School districts may contribute toward:

- Healthcare premiums

- Pension system funding

- Retiree healthcare eligibility

Step 4: Retirement Income Transition

In retirement, income typically shifts to:

- Monthly pension payments

- Social Security (if eligible)

- Investment withdrawals

- Part-time work (optional)

How to Maximize Teacher Retirement Benefits

A strong retirement strategy focuses on coordination, not just accumulation.

Step 1: Understand Your Pension Estimate

Review:

- Service credit accuracy

- Final salary assumptions

- Retirement age impact

Step 2: Increase Supplemental Savings Early

Small increases in 403(b) or 457(b) contributions can significantly improve long-term outcomes.

Step 3: Plan for Healthcare Costs

Include:

- Medicare premiums (if applicable)

- Out-of-pocket medical expenses

- Retiree health plan coverage gaps

Step 4: Coordinate Income Sources

Balance:

- Pension income

- Social Security

- Savings withdrawals

Step 5: Reassess Regularly

Annual reviews help adjust for inflation, policy changes, and life events.

Warning Signs Your Teacher Retirement Plan Needs Attention

Many educators underestimate how early planning impacts retirement stability.

Watch for these signals:

- You don’t know your estimated pension amount.

- You have not increased retirement contributions recently.

- You are within 5–10 years of retirement.

- You rely solely on pension income.

- You have not planned for healthcare inflation.

- You are unsure about Social Security eligibility.

- You carry debt approaching retirement.

Early awareness helps prevent financial stress later.

Frequently Asked Questions

Are teacher retirement benefits enough to retire comfortably?

For some educators, yes—but many still rely on supplemental savings to cover healthcare costs, inflation, and lifestyle needs.

When should teachers start planning for retirement?

Ideally within the first 5–10 years of teaching, though it is never too late to improve retirement readiness.

Do all teachers get Social Security in retirement?

No. Eligibility depends on whether the teacher paid into Social Security during other employment or worked in covered positions.

Final Thoughts

Teacher retirement benefits form a strong foundation—but they are not a complete picture on their own. A secure retirement depends on how well pensions, savings, healthcare coverage, and Social Security are coordinated.

The most successful retirement plans are built gradually through consistent contributions, informed decisions, and regular reviews. Even small adjustments today can significantly improve financial stability in the future.

After years of dedication in the classroom, teachers deserve a retirement that feels stable, predictable, and well-prepared—not uncertain or reactive.