Having a low credit score can feel like every financial door is closed. Whether you’re dealing with unexpected medical bills, car repairs, or trying to consolidate debt, finding loans for bad credit often comes with higher interest rates, stricter requirements, and unfortunately, more scams.

The good news is that bad credit doesn’t automatically mean you have no borrowing options. Many lenders now look beyond your credit score by considering your income, employment history, and ability to repay. Understanding your choices before applying can save you hundreds—or even thousands—of dollars over the life of a loan.

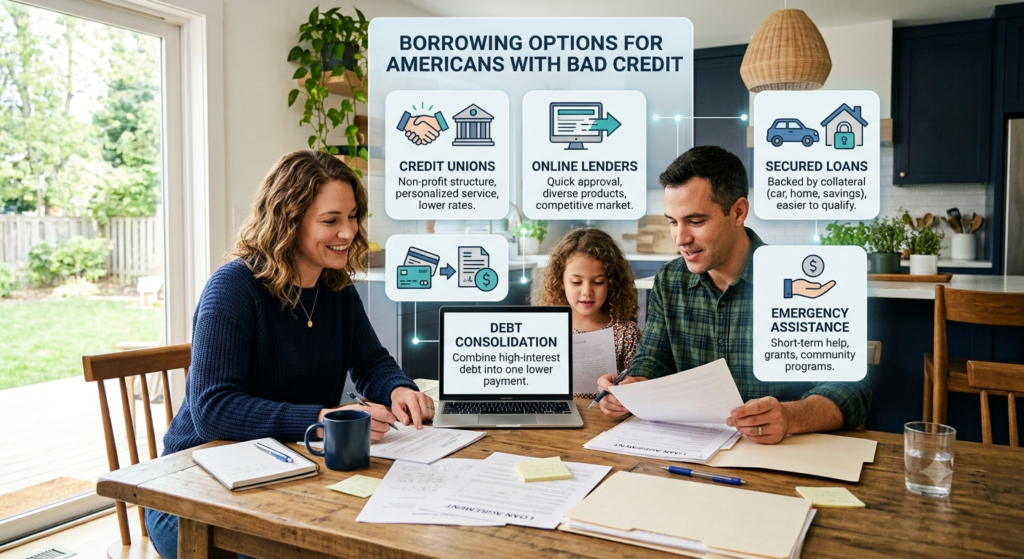

Types of Loans for Bad Credit

Not every loan is created equal. Choosing the right type depends on why you need the money and how quickly you can repay it.

- Personal Installment Loans

- Fixed monthly payments

- Borrow from approximately $1,000 to $50,000

- Typically repaid over 2–7 years

- Secured Loans

- Require collateral such as a vehicle or savings account

- Easier approval for borrowers with poor credit

- Lower interest rates than unsecured loans

- Credit Union Loans

- Often offer lower rates and flexible underwriting

- May include Payday Alternative Loans (PALs)

- Ideal for existing members

- Co-Signed Loans

- A family member or trusted friend helps strengthen the application

- Can significantly improve approval odds

- Both borrowers share repayment responsibility

- Debt Consolidation Loans

- Combine multiple debts into one payment

- May lower monthly payments if qualified

- Helpful for organizing finances

- Online Bad Credit Loans

- Fast application process

- Funding may arrive within one business day

- Compare multiple lenders carefully before accepting an offer

What Loans for Bad Credit Actually Cost in 2026

The total cost of borrowing depends on your credit score, income, loan amount, and lender policies.

Typical borrowing costs include:

| Loan Type | Typical APR (2026) | Loan Amount |

|---|---|---|

| Credit Union Loan | 8%–18% | $500–$20,000 |

| Personal Loan | 12%–36% | $1,000–$50,000 |

| Secured Loan | 7%–20% | Varies |

| Payday Loan | Equivalent APR often exceeds 300% | $100–$1,000 |

Borrowers living in California, New York, Massachusetts, and other higher-cost states may find larger loan amounts available but often face stricter income verification. In many rural communities, local banks and credit unions may offer more personalized lending decisions.

Besides interest, borrowers should watch for:

- Origination fees

- Late payment penalties

- Prepayment restrictions

- Returned payment fees

💡 Tip/Note Box

Cost-Saving Tip: Before accepting any loan, compare the Annual Percentage Rate (APR) instead of focusing only on the monthly payment. A lower monthly payment can sometimes mean paying substantially more interest over time.

How to Pay for It / Financial Options

If you’re approved for a loan, borrowing should ideally solve a temporary financial problem—not create a larger one.

Consider these financing options before accepting a high-interest loan.

Credit Unions

Many credit unions offer affordable lending programs specifically designed for members with limited or damaged credit histories.

Community Development Financial Institutions (CDFIs)

CDFIs specialize in serving underserved communities and may provide more flexible approval requirements.

Employer Assistance Programs

Some employers now provide paycheck advances or emergency loan programs with minimal or no interest.

Family Loans

Borrowing from trusted family members can eliminate expensive interest charges if repayment expectations are clearly documented.

Veterans Benefits

Eligible veterans may qualify for emergency financial assistance through veteran support organizations depending on their circumstances.

Emergency Assistance Programs

Before borrowing, check whether local nonprofits, charities, or state assistance programs can help cover emergency expenses like rent, utilities, or medical bills.

How to Choose the Right Lender

Finding the right lender is just as important as finding the right loan.

Use this checklist before signing any agreement.

✔ Compare Multiple Offers

Never accept the first offer you receive. Comparing several lenders may reveal dramatically different interest rates and fees.

✔ Verify Licensing

Confirm that the lender is authorized to operate in your state.

✔ Read Customer Reviews

Look for consistent feedback about customer service, hidden fees, and repayment flexibility.

✔ Understand Every Fee

Ask about:

- Origination fees

- Late charges

- Early payoff penalties

- Automatic payment discounts

✔ Review the Repayment Schedule

Choose payments that comfortably fit your monthly budget instead of stretching your finances.

✔ Watch for Scams

Avoid lenders who:

- Guarantee approval before reviewing your information

- Require upfront fees

- Pressure you to act immediately

- Ask for payment through gift cards or cryptocurrency

Signs It’s Time to Consider a Bad Credit Loan

A loan should support your financial stability—not become a recurring habit.

You may benefit from a carefully selected loan if:

- An emergency expense cannot be delayed

- You have reliable monthly income

- You can comfortably afford the monthly payments

- The loan replaces more expensive debt

- You’ve already explored grants, assistance programs, and savings

You may want to wait if:

- You’re borrowing for discretionary spending.

- You’re already struggling to make existing debt payments.

- You don’t have a realistic repayment plan.

Frequently Asked Questions

Can I get a loan with a credit score below 600?

Yes. Many lenders consider applicants with scores below 600, especially if they have stable income and manageable debt.

Will applying for several loans hurt my credit?

Multiple hard inquiries within a short shopping period for the same type of loan are often treated as a single inquiry by many credit scoring models. Compare lenders within a focused time frame.

Should I use a payday loan if I have no other option?

Payday loans generally carry extremely high borrowing costs and short repayment periods. They should typically be considered only after exploring safer alternatives such as credit unions, employer assistance, payment plans, or community financial programs.

Final Thoughts

Needing loans for bad credit doesn’t mean you’re out of options. The key is to borrow thoughtfully, compare lenders carefully, and understand the true cost of financing before signing any agreement.

The strongest loan isn’t always the one with the fastest approval—it’s the one that helps you solve today’s financial challenge without creating tomorrow’s. By focusing on affordable payments, transparent terms, and reputable lenders, you can make a borrowing decision that supports your long-term financial health rather than undermining it.