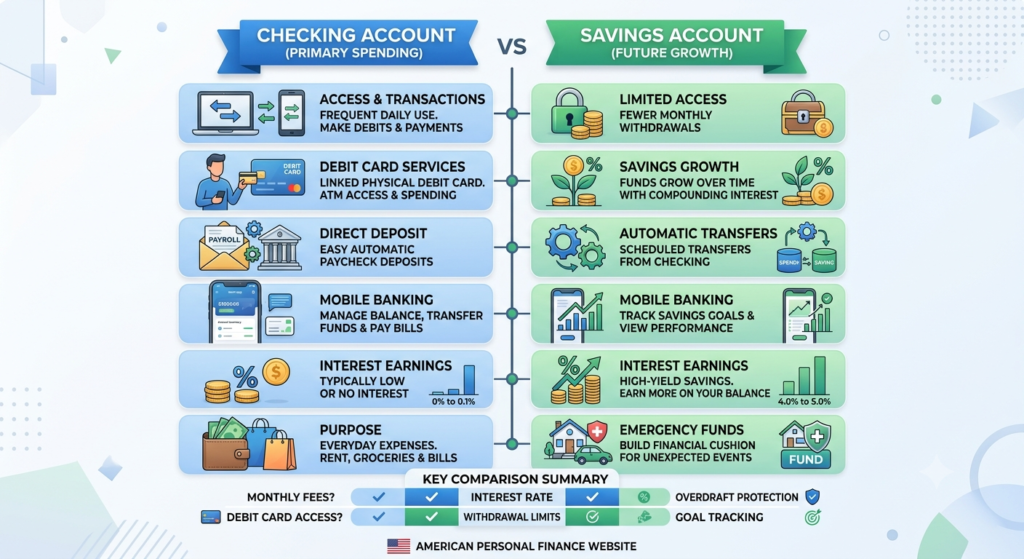

Managing your money starts with choosing the right bank account. If you’re trying to compare checking and savings accounts, understanding how each account works can help you make better financial decisions. Although both accounts allow you to store your money safely, they serve different purposes.

A checking account is designed for everyday spending and frequent transactions, while a savings account helps you build financial security by earning interest on money you plan to keep for future needs. Knowing when to use each account—and how they complement one another—can improve your budgeting and long-term financial health.

This guide explains the differences, benefits, and key features of checking and savings accounts so you can select the best option for your lifestyle.

What Is a Checking Account?

A checking account is intended for everyday banking activities. It provides quick access to your money and supports frequent transactions.

Typical features include:

- Debit card purchases

- Online bill payments

- ATM withdrawals

- Direct deposit

- Mobile check deposit

- Digital banking tools

Checking accounts are ideal for receiving paychecks, paying monthly bills, shopping, and handling everyday expenses. Many accounts have little or no interest, but they offer maximum flexibility.

What Is a Savings Account?

A savings account is designed to help you set aside money while earning interest. Unlike checking accounts, savings accounts encourage saving rather than frequent spending.

Savings accounts are commonly used for:

- Emergency funds

- Vacation savings

- Home down payments

- Education expenses

- Holiday spending

- Future investments

Many online financial institutions offer high-yield savings accounts that provide significantly higher annual percentage yields (APYs) than traditional savings accounts.

Compare Checking and Savings Accounts

Understanding the differences makes it easier to select the right account for your financial needs.

| Feature | Checking Account | Savings Account |

|---|---|---|

| Primary purpose | Daily spending | Saving money |

| Debit card | Yes | Sometimes |

| Bill payments | Yes | Limited |

| Interest earnings | Occasionally | Usually |

| ATM access | Frequent | Limited |

| Monthly transactions | Unlimited at most banks | May have limits |

| Best for | Everyday expenses | Financial goals |

Both accounts are insured by eligible financial institutions, making them safe places to store your money.

Advantages of a Checking Account

Checking accounts are ideal if you need regular access to your funds.

Benefits include:

- Fast access to cash

- Easy bill payments

- Payroll direct deposit

- Convenient debit card purchases

- Online and mobile banking

- Wide ATM availability

Because these accounts support frequent transactions, they are the foundation of most personal banking plans.

Advantages of a Savings Account

Savings accounts help you prepare for future financial needs.

Key advantages include:

- Earn interest on your balance

- Build an emergency fund

- Separate savings from spending

- Encourage better budgeting

- Reduce unnecessary impulse purchases

Keeping savings separate from your checking account can make it easier to achieve long-term financial goals.

Which Account Should You Choose?

The answer depends on how you plan to use your money.

A checking account is best if you:

- Pay bills regularly

- Receive direct deposits

- Use a debit card frequently

- Need daily access to funds

A savings account is better if you:

- Want to earn interest

- Build an emergency fund

- Save for future purchases

- Separate spending from savings

For most people, using both accounts together provides the greatest flexibility and financial control.

Tips for Using Both Accounts Effectively

Combining checking and savings accounts can strengthen your financial habits.

Consider these strategies:

- Deposit your paycheck into your checking account.

- Schedule automatic transfers to savings every payday.

- Keep three to six months of living expenses in an emergency fund.

- Monitor account balances using mobile banking alerts.

- Review fees and interest rates annually to ensure you’re getting the best value.

- Avoid overdraft fees by maintaining a buffer in your checking account.

These simple habits can improve your financial stability and make it easier to achieve both short-term and long-term goals.

Frequently Asked Questions

Can I have both a checking and savings account?

Yes. Many people use a checking account for daily expenses and a savings account for emergencies and future financial goals.

Which account earns more interest?

Savings accounts generally offer higher interest rates than checking accounts, especially high-yield savings accounts.

Are checking accounts safe?

Yes. Accounts at FDIC-insured banks or NCUA-insured credit unions are protected up to applicable insurance limits.

Can I transfer money between accounts?

Yes. Most banks allow instant transfers between linked checking and savings accounts through online or mobile banking.

Is there a minimum balance requirement?

It depends on the financial institution. Some accounts have no minimum balance, while others require a minimum to avoid monthly fees or earn the highest interest rate.

Final Thoughts

When you compare checking and savings accounts, it becomes clear that each serves a unique purpose. A checking account provides convenient access for everyday transactions, while a savings account helps you grow your money through interest and supports long-term financial planning.

Rather than choosing one over the other, many consumers benefit from using both. By pairing a checking account for routine spending with a savings account for future goals, you can improve budgeting, reduce financial stress, and build a stronger financial foundation in 2026.