Losing employer-sponsored health insurance can be stressful, especially when you still need medical coverage for yourself or your family. COBRA insurance gives many employees and their dependents the option to continue their existing employer health plan for a limited time after certain life events, such as leaving a job or experiencing a reduction in work hours.

While COBRA can help prevent gaps in healthcare coverage, it often comes with higher monthly premiums because you’ll typically pay the full cost of the plan. Understanding how COBRA works, who qualifies, and what alternatives are available can help you make an informed decision.

In this guide, we’ll explain the basics of COBRA insurance, its eligibility requirements, costs, enrollment process, and situations where it may be the right choice.

What Is COBRA Insurance?

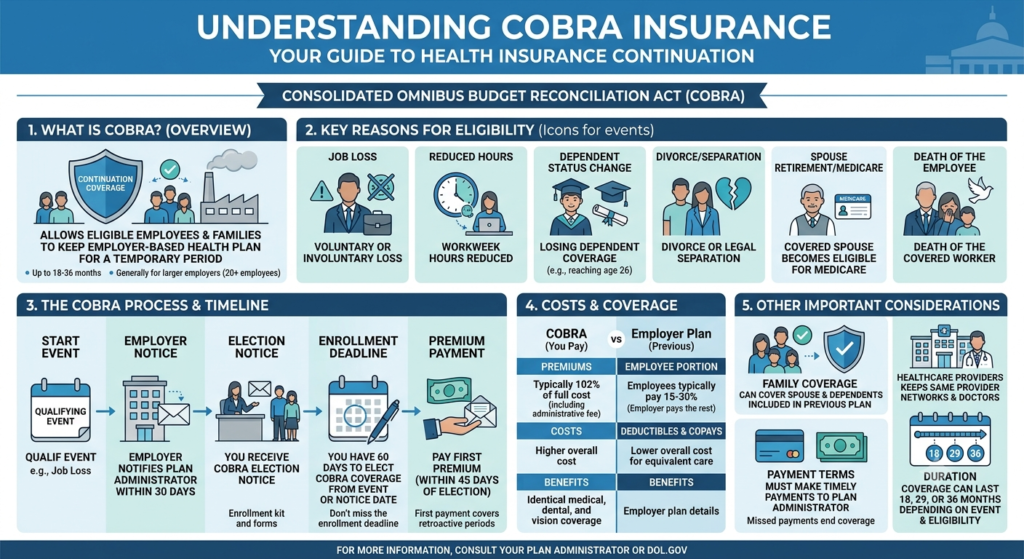

COBRA insurance refers to health coverage available under the Consolidated Omnibus Budget Reconciliation Act (COBRA). This federal law allows eligible employees and their qualified beneficiaries to temporarily continue their employer-sponsored group health insurance after certain qualifying events.

Rather than switching immediately to a new health plan, eligible individuals can generally keep the same doctors, hospitals, and benefits they already use under their employer’s health plan.

Common qualifying events include:

- Voluntary or involuntary job loss (excluding certain cases involving gross misconduct)

- Reduction in work hours

- Retirement

- Divorce or legal separation

- Death of the covered employee

- A dependent child losing eligibility under the employer’s plan

Who Is Eligible for COBRA?

Eligibility depends on both the employer and the qualifying event.

Generally, COBRA applies to private-sector employers and many state and local government employers with 20 or more employees that offer group health plans.

Qualified beneficiaries may include:

- Employees

- Spouses

- Former spouses

- Dependent children

After a qualifying event, the employer or health plan administrator provides a COBRA election notice explaining your continuation coverage rights and enrollment deadlines.

How COBRA Insurance Works

Once you become eligible, you’ll have a limited window to elect COBRA continuation coverage.

If you choose COBRA:

- Your health coverage generally remains the same.

- You can continue using your current provider network.

- Covered family members may also remain on the plan if eligible.

- Coverage is usually temporary and lasts for a specified period, depending on the qualifying event.

One important difference is cost. While employed, your employer may have paid a significant portion of your health insurance premium. Under COBRA, you’ll generally pay the entire premium yourself, plus a small administrative fee allowed by law.

What Does COBRA Insurance Cost?

The biggest drawback of COBRA insurance is often the monthly premium.

Because employer contributions typically end after employment, you’ll usually be responsible for:

- The full monthly premium

- A permitted administrative fee

Although the premium may be higher than what you paid as an employee, keeping your existing coverage may be worthwhile if you’re in the middle of treatment, have established healthcare providers, or expect ongoing medical expenses.

| Feature | COBRA Insurance |

|---|---|

| Keep existing health plan | ✔ |

| Continue current doctors | Usually |

| Employer contribution | Typically ends |

| Monthly premium | Usually higher |

| Temporary coverage | Yes |

Advantages of COBRA Insurance

Many people choose COBRA because it provides continuity during major life transitions.

Benefits include:

- No interruption in healthcare coverage

- Keep your current doctors and specialists

- Continue existing prescription drug coverage

- No need to change treatment plans immediately

- Coverage available for eligible family members

For individuals undergoing ongoing medical treatment, maintaining consistent coverage can be especially valuable.

Alternatives to COBRA Insurance

Although COBRA works well for many individuals, it isn’t the only option.

Possible alternatives include:

- Marketplace health insurance plans

- Medicaid, if you qualify based on income and state eligibility rules

- Medicare, if you’re eligible

- A spouse’s employer-sponsored health plan

- Individual health insurance purchased directly from an insurer

Comparing premiums, deductibles, provider networks, and prescription coverage can help determine the best choice for your situation.

Tips Before Choosing COBRA

Before enrolling, consider the following:

- Compare total monthly costs with other available plans.

- Review deductibles and out-of-pocket expenses.

- Confirm your preferred doctors participate in alternative plans.

- Check prescription medication coverage.

- Be aware of enrollment deadlines to avoid losing your continuation rights.

Evaluating both cost and coverage ensures you choose a plan that meets your healthcare and financial needs.

Frequently Asked Questions

How long does COBRA insurance last?

The length of COBRA continuation coverage depends on the qualifying event and applicable rules. In many cases, coverage lasts up to 18 months, though certain situations may allow longer continuation periods.

Can my family stay on COBRA?

Yes. Qualified spouses and dependent children may also be eligible to continue coverage under the employer’s health plan.

Is COBRA cheaper than buying private insurance?

Not always. Because you’ll generally pay the full premium, comparing COBRA with Marketplace plans and other options is important before making a decision.

Can I cancel COBRA early?

Yes. You may terminate COBRA coverage if you obtain other qualifying health insurance or no longer wish to continue the plan, subject to the plan’s terms.

Do I need to reapply for my doctors?

Typically no. Since COBRA usually continues your existing employer-sponsored health plan, you can generally continue seeing providers already included in your plan’s network.

Final Thoughts

COBRA insurance offers an important safety net for individuals and families facing the loss of employer-sponsored health coverage. By allowing eligible participants to temporarily continue their existing health plan, COBRA helps reduce disruptions in medical care and provides valuable continuity during periods of job transition or other qualifying life events.

Before enrolling, carefully compare COBRA with Marketplace plans, Medicaid, Medicare, or other available options. Reviewing premiums, coverage, provider networks, and enrollment deadlines will help you choose the health insurance solution that best supports your healthcare needs and financial goals in 2026.