Paying for college often requires financial assistance, and federal student loans remain one of the most common ways to cover education costs. When comparing subsidized vs unsubsidized student loans, understanding how interest, eligibility, and repayment differ can help you make informed borrowing decisions.

Both loan types are offered through the U.S. Department of Education and provide valuable funding for eligible students. However, one major difference can significantly affect the total amount you repay over time: who pays the interest while you’re in school.

This guide explains the differences between subsidized and unsubsidized student loans, their advantages, and how to determine which option best fits your financial situation.

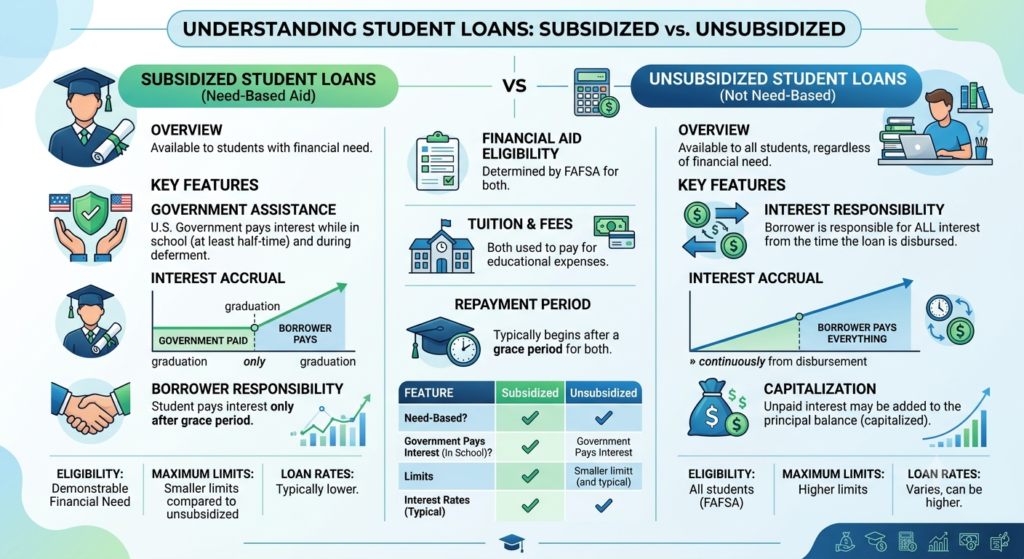

What Are Subsidized Student Loans?

Subsidized student loans are federal loans available to undergraduate students who demonstrate financial need. One of their biggest advantages is that the federal government pays the interest during certain periods.

Generally, the government covers interest while you:

- Are enrolled at least half-time

- Are within the grace period after leaving school

- Qualify for certain authorized deferment periods

Because interest does not accumulate during these qualifying periods, subsidized loans usually cost less over the life of the loan.

What Are Unsubsidized Student Loans?

Unsubsidized student loans are also federal loans, but they are available to a broader range of students.

Unlike subsidized loans:

- Financial need is not required.

- Undergraduate and graduate students may qualify, depending on current federal program rules.

- Interest begins accruing as soon as the loan is disbursed.

Although you can postpone making payments while you’re in school, unpaid interest may be added to your loan balance if it is capitalized, increasing the total amount you’ll repay.

Subsidized vs Unsubsidized Student Loans

Here’s a side-by-side comparison of the two federal loan types.

| Feature | Subsidized Loan | Unsubsidized Loan |

|---|---|---|

| Financial need required | Yes | No |

| Available to undergraduates | Yes | Yes |

| Available to graduate students | No | Yes (subject to federal rules) |

| Interest while in school | Paid by government during eligible periods | Borrower responsible |

| Total borrowing cost | Usually lower | Usually higher |

The biggest distinction is interest. Because subsidized loans receive an interest subsidy during qualifying periods, borrowers often save money over time.

Which Loan Should You Choose?

If you’re eligible for subsidized loans, they are generally the first option to consider because they reduce interest costs.

However, many students use both loan types to help pay for:

- Tuition

- Housing

- Books

- Meal plans

- School supplies

- Transportation

Your financial aid award may include a combination of grants, scholarships, work-study opportunities, subsidized loans, and unsubsidized loans.

Borrow only what you need, even if you’re offered a larger amount.

Benefits of Federal Student Loans

Federal student loans offer several advantages compared to many private student loans.

Benefits may include:

- Fixed interest rates

- Flexible repayment plans

- Income-driven repayment options for eligible borrowers

- Deferment and forbearance opportunities

- Potential loan forgiveness programs for qualifying borrowers

Understanding these benefits can help you manage repayment after graduation.

Smart Borrowing Tips

Regardless of which loan you receive, responsible borrowing can reduce future financial stress.

Consider these strategies:

- Complete the FAFSA as early as possible each year.

- Accept grants and scholarships before borrowing.

- Prioritize subsidized loans if eligible.

- Borrow only the amount needed for educational expenses.

- Pay interest on unsubsidized loans while in school if possible.

- Create a repayment plan before graduation.

Small financial decisions during college can have a significant impact after graduation.

Frequently Asked Questions

Which loan is better: subsidized or unsubsidized?

Subsidized loans are generally considered more affordable because the government pays interest during certain qualifying periods, reducing the total borrowing cost.

Do unsubsidized loans require financial need?

No. Eligibility for unsubsidized federal student loans is not based on financial need.

Can I receive both loan types?

Yes. Many eligible undergraduate students receive both subsidized and unsubsidized federal student loans as part of their financial aid package.

When does repayment begin?

Most federal student loans provide a grace period after leaving school or dropping below half-time enrollment before regular payments begin, although interest rules differ between loan types.

Can graduate students receive subsidized loans?

No. Under current federal rules, subsidized Direct Loans are available only to eligible undergraduate students who demonstrate financial need.

Final Thoughts

Understanding subsidized vs unsubsidized student loans is essential when planning how to finance your education. While both loan types provide valuable federal funding, subsidized loans typically offer greater long-term savings because the government pays interest during certain qualifying periods.

Before accepting any student loan, review your financial aid package carefully, estimate your future repayment obligations, and borrow only what you truly need. Combining scholarships, grants, part-time work, and responsible borrowing can help minimize debt while allowing you to focus on achieving your educational goals.