Healthcare costs are one of the biggest financial concerns facing retirees and public employees today. Even families who have carefully prepared for retirement often find themselves overwhelmed by plan choices, premium differences, provider networks, and questions about Medicare coordination.

For California public employees and retirees, CalPERS health plans provide access to a wide range of medical coverage options. But choosing the right plan isn’t always straightforward. The wrong decision can lead to higher costs, limited provider access, or unexpected out-of-pocket expenses.

This guide explains how CalPERS health plans work, what they typically cost in 2026, and how families can confidently choose the coverage that best fits their healthcare and financial needs.

Types of CalPERS Health Plans

CalPERS offers several healthcare coverage options designed to meet different medical and financial needs.

Common CalPERS Health Plan Categories

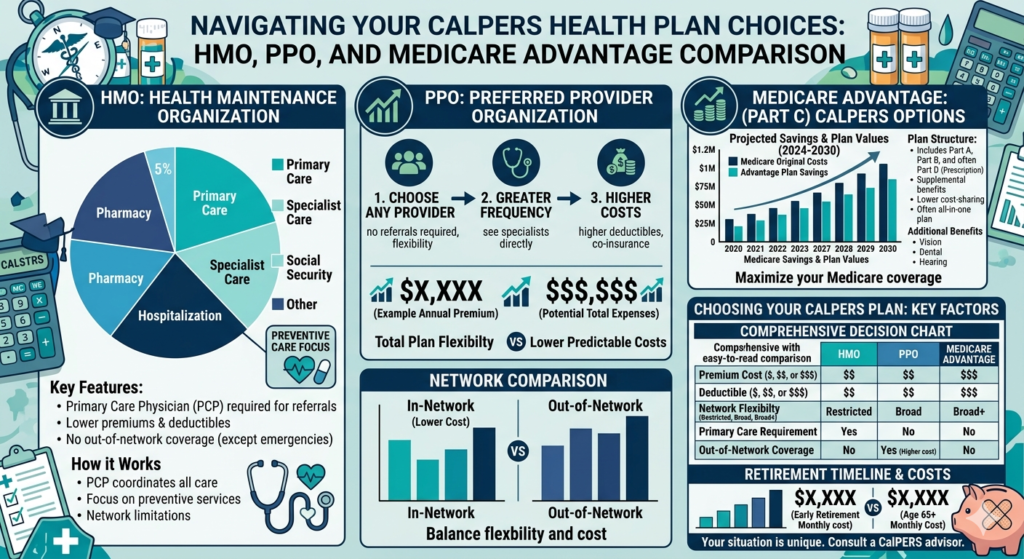

- Health Maintenance Organization (HMO) PlansTypically require members to use a network of physicians and hospitals. These plans often feature lower out-of-pocket costs and coordinated care.

- Preferred Provider Organization (PPO) PlansOffer greater flexibility to see specialists and providers both inside and outside the network, usually at higher costs.

- Medicare Advantage PlansAvailable to eligible retirees enrolled in Medicare. These plans combine Medicare benefits with additional services and coordinated coverage.

- Medicare Supplement Coordination PlansWork alongside Medicare to help reduce deductibles, copayments, and other healthcare expenses.

- Basic Plans for Active EmployeesDesigned for current state and public agency employees who are not yet Medicare eligible.

- Retiree Health PlansCoverage specifically structured for retired members and their dependents.

Each plan type comes with different premium levels, provider networks, prescription drug coverage, and cost-sharing requirements.

What CalPERS Health Plans Actually Cost in 2026

One of the most important factors when selecting coverage is understanding the true cost beyond monthly premiums.

Typical Monthly Premium Ranges in 2026

Depending on plan type, geographic region, and employer contributions, members may see monthly costs such as:

| Coverage Type | Estimated Monthly Premium |

|---|---|

| Employee Only | $0–$400+ |

| Employee + Spouse | $200–$900+ |

| Family Coverage | $400–$1,500+ |

| Medicare Retiree Plans | $0–$500+ |

Actual costs vary significantly depending on employer contributions and the specific CalPERS plan selected.

Other Healthcare Expenses

Families should also budget for:

- Copayments

- Deductibles

- Coinsurance

- Prescription drug costs

- Specialist visits

- Out-of-network services (for PPO plans)

Regional Cost Differences

Healthcare expenses can vary considerably.

Members living in high-cost healthcare markets such as Los Angeles, San Francisco, San Diego, and parts of New York often face higher medical service costs than individuals living in rural communities or lower-cost regions.

[💡 Tip/Note Box]

Don’t focus exclusively on premiums. A plan with a slightly higher monthly premium may save thousands of dollars annually if it offers lower deductibles, broader provider access, or better prescription drug coverage.

How to Pay for It / Financial Options

Healthcare coverage often involves multiple funding sources working together.

Employer Contributions

Many active employees receive employer contributions that significantly reduce monthly premium costs.

The amount varies by:

- Employer

- Bargaining agreement

- Employment classification

- Coverage level

Retiree Health Benefits

Some retirees qualify for employer-sponsored retiree health contributions that continue after retirement.

Eligibility typically depends on:

- Years of service

- Retirement status

- Employer participation

Medicare

For retirees age 65 and older, Medicare becomes a critical component of healthcare coverage.

Medicare may include:

- Part A (Hospital Insurance)

- Part B (Medical Insurance)

- Part D (Prescription Drug Coverage)

- Medicare Advantage Plans

Many CalPERS retiree plans coordinate directly with Medicare.

Private Savings

Even with insurance coverage, families should prepare for:

- Copays

- Deductibles

- Non-covered services

- Dental and vision expenses

Dedicated healthcare savings can help prevent unexpected financial strain.

Veterans Benefits

Eligible veterans may access healthcare support through federal programs, potentially reducing overall healthcare costs.

How to Choose a CalPERS Health Plan

The best plan depends on your healthcare needs, budget, and preferred providers.

Step 1: Review Your Healthcare Usage

Ask:

- How often do I visit doctors?

- Do I see specialists regularly?

- Do I take expensive medications?

Step 2: Verify Provider Networks

Before enrolling:

- Confirm primary care physician participation

- Verify specialist access

- Check hospital affiliations

Step 3: Compare Total Annual Costs

Calculate:

- Premiums

- Deductibles

- Copays

- Prescription costs

The lowest premium isn’t always the most affordable option overall.

Step 4: Evaluate Medicare Coordination

Medicare-eligible retirees should carefully compare:

- Medicare Advantage options

- Supplemental coverage

- Prescription drug benefits

Step 5: Review Annual Open Enrollment Materials

Plan offerings, costs, and provider networks may change from year to year.

Conduct a fresh review during every enrollment period.

Signs It’s Time to Consider Reviewing Your CalPERS Health Plan

Healthcare needs change over time.

Review your plan if any of these situations apply:

- Your doctor is no longer in-network.

- Prescription drug costs have increased significantly.

- You recently became Medicare eligible.

- You have developed new chronic health conditions.

- Your healthcare usage has increased.

- Your spouse’s healthcare needs have changed.

- Premiums have risen substantially.

- You have not compared plans during the last enrollment cycle.

Regular reviews can help prevent unnecessary expenses and ensure continued access to quality care.

Frequently Asked Questions

Are CalPERS health plans only available to retirees?

No. CalPERS health plans are available to eligible active employees, retirees, and qualifying dependents through participating public employers.

What happens to my CalPERS health plan when I turn 65?

Most members become eligible for Medicare and may need to enroll in Medicare Parts A and B to maintain certain CalPERS retiree health benefits.

Is an HMO or PPO better under CalPERS?

Neither is universally better. HMOs often offer lower costs and coordinated care, while PPOs provide greater provider flexibility and broader access to specialists.

Final Thoughts

Choosing among CalPERS health plans is one of the most important healthcare and financial decisions California public employees and retirees will make. The right plan can help control costs, simplify access to care, and provide peace of mind during retirement.

While comparing premiums is important, families should also evaluate provider networks, prescription drug coverage, Medicare coordination, and expected healthcare usage. A thoughtful review today can help avoid costly surprises tomorrow.

Healthcare decisions are rarely simple, but understanding your CalPERS options can make the process far more manageable and help ensure you receive the coverage you need throughout every stage of life.