For many California educators, retirement planning can feel surprisingly complicated. You may already contribute to a CalSTRS pension, but you’re also hearing that a 403(b) account is essential for building additional retirement security. The challenge is figuring out how these two retirement tools work together—and whether you’re saving enough for the future.

The reality is that while a CalSTRS pension provides valuable guaranteed income, many retirees discover that pensions alone may not fully cover healthcare costs, inflation, travel goals, or unexpected expenses. That’s where a 403(b) can play a powerful supporting role.

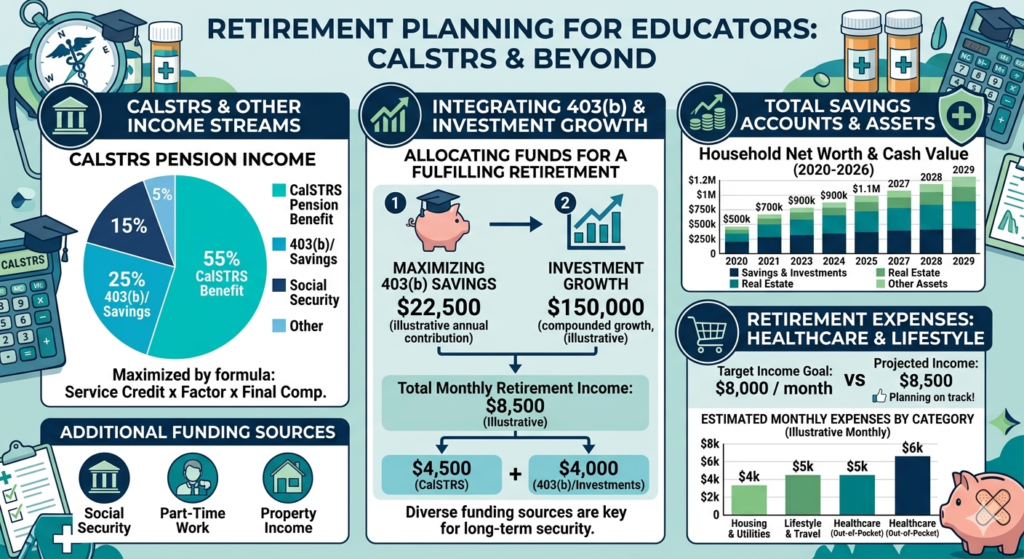

This guide explains how CalSTRS and 403(b) plans fit together, what they cost, how to maximize their benefits, and how to determine whether your current retirement strategy is on track in 2026.

Types of CalSTRS and 403(b) Plans

Although both are retirement tools, they serve very different purposes.

Understanding the Main Components

- CalSTRS Defined-Benefit PensionProvides guaranteed lifetime monthly income based on years of service, age at retirement, and compensation history.

- Traditional 403(b) PlansAllow educators to contribute pre-tax dollars, lowering current taxable income while building retirement savings.

- Roth 403(b) PlansContributions are made with after-tax dollars, allowing qualified withdrawals to be tax-free in retirement.

- Fixed Annuity 403(b) InvestmentsOffer stable returns and lower risk but generally lower growth potential.

- Mutual Fund 403(b) InvestmentsProvide diversified market exposure with potentially higher long-term growth.

- 403(b) Catch-Up ContributionsAdditional contribution opportunities available for certain employees nearing retirement.

Understanding the differences helps educators create a retirement plan that balances guaranteed income with growth potential.

What CalSTRS and 403(b) Actually Cost in 2026

Unlike long-term care or healthcare services, retirement planning costs are often hidden in contributions, fees, and investment expenses.

Typical CalSTRS Contributions

Most active California educators contribute a percentage of salary directly into CalSTRS.

For a teacher earning:

| Annual Salary | Approximate Employee Contribution |

|---|---|

| $60,000 | $6,000–$7,000 |

| $80,000 | $8,000–$9,000 |

| $100,000 | $10,000–$11,000 |

Actual contribution rates vary based on employment classification and district policies.

Typical 403(b) Contributions

Educators choose how much to contribute.

Common contribution ranges include:

- $100–$300 monthly for early-career educators

- $300–$800 monthly for mid-career educators

- $800–$2,000+ monthly for educators nearing retirement

The IRS contribution limit for 403(b) plans in 2026 may be adjusted annually for inflation, making it important to review current limits each year.

Investment Fees Matter

403(b) plan costs may include:

- Administrative fees

- Investment management fees

- Mutual fund expense ratios

- Annuity contract charges

High fees can significantly reduce long-term retirement growth.

[💡 Tip/Note Box]

A difference of just 1% in annual investment fees can potentially reduce retirement savings by tens of thousands of dollars over a 20- to 30-year career. Always review fee disclosures before selecting a 403(b) provider.

Regional Considerations

Educators planning retirement in high-cost areas such as Los Angeles, San Francisco, San Diego, or New York often need larger supplemental savings accounts than retirees relocating to lower-cost regions or rural communities.

How to Pay for It / Financial Options

The goal is not choosing between CalSTRS and a 403(b). Most educators benefit from using both.

CalSTRS Pension

The pension serves as the retirement foundation by providing predictable monthly income for life.

Benefits include:

- Lifetime payments

- Survivor options

- Inflation protection mechanisms

- Reduced market risk

403(b) Contributions

A 403(b) can help pay for:

- Healthcare expenses

- Travel goals

- Home repairs

- Inflation-related spending increases

- Unexpected emergencies

Roth 403(b) Option

Many younger educators choose Roth contributions because:

- Future withdrawals may be tax-free

- Retirement tax rates are uncertain

- Long investment horizons support growth

IRA Contributions

Some educators also contribute to:

- Traditional IRAs

- Roth IRAs

These accounts can provide additional tax diversification.

Health Savings Accounts (HSAs)

For educators eligible through qualified health plans, HSAs offer valuable tax advantages and can supplement retirement healthcare funding.

How to Choose a 403(b) Provider

Not all 403(b) plans are equal.

Use this step-by-step checklist when evaluating providers.

Step 1: Compare Fees

Request written disclosure of:

- Administrative fees

- Expense ratios

- Advisory fees

- Surrender charges

Step 2: Review Investment Choices

Look for:

- Broad stock index funds

- Bond funds

- Target-date retirement funds

- Low-cost diversified portfolios

Step 3: Evaluate Provider Reputation

Research:

- Years in business

- Customer service reviews

- Financial strength ratings

Step 4: Understand Withdrawal Rules

Verify:

- Early withdrawal penalties

- Loan provisions

- Distribution flexibility

Step 5: Consider Professional Guidance

A fiduciary financial advisor can help determine whether your contributions align with retirement goals.

Signs It’s Time to Increase Your Retirement Planning Efforts

Many educators assume their pension alone will cover retirement needs.

These warning signs suggest a closer review may be necessary:

- You have not increased 403(b) contributions in several years.

- You are within ten years of retirement.

- You do not know your projected CalSTRS retirement benefit.

- You carry significant debt approaching retirement.

- You have little savings outside your pension.

- Healthcare costs are becoming a larger share of your budget.

- You have not reviewed investment fees recently.

- You are unsure whether your retirement income will keep pace with inflation.

Taking action earlier generally creates more flexibility and less stress later.

Frequently Asked Questions

Is CalSTRS enough for retirement by itself?

For some educators, yes. However, many retirees use a 403(b) to supplement pension income and address rising healthcare costs, inflation, and lifestyle goals.

Should I contribute to a 403(b) if I already have a pension?

In many cases, yes. A 403(b) provides additional savings, investment growth potential, and flexibility that a pension alone may not offer.

Which is better: Traditional 403(b) or Roth 403(b)?

It depends on your current tax bracket, expected retirement income, and long-term goals. Many educators benefit from a combination of both tax strategies.

Final Thoughts

CalSTRS and 403(b) plans are not competing retirement tools—they are designed to work together. Your pension provides dependable lifetime income, while a 403(b) offers flexibility, growth potential, and protection against future financial uncertainty.

The most successful retirement plans typically combine guaranteed pension benefits with consistent supplemental savings. Whether retirement is five years away or thirty, understanding how CalSTRS and 403(b) accounts complement one another can help you make more confident financial decisions.

Retirement security is rarely built through a single account. It’s built through a thoughtful strategy that evolves with your career, your family, and your future goals.