Retirement planning often comes down to one critical question: Will Social Security be enough? For millions of Americans, Social Security benefits represent a major source of retirement income. Yet many families are surprised by how complex the system can be when it comes to eligibility, claiming age, survivor benefits, taxes, and monthly payment amounts.

Whether you’re approaching retirement, helping aging parents, or planning decades ahead, understanding your Social Security Benefit options can have a significant impact on your financial security. The good news is that a few informed decisions today can potentially increase lifetime benefits by tens of thousands of dollars.

Types of Social Security Benefits

Many people associate Social Security only with retirement, but the program provides several different types of benefits.

Common Categories of Social Security Benefits

- Retirement BenefitsMonthly payments based on your lifetime earnings and work history. Most Americans qualify after earning sufficient work credits throughout their careers.

- Spousal BenefitsEligible spouses may receive benefits based on a current or former spouse’s earnings record, even if they have limited work history themselves.

- Survivor BenefitsWidows, widowers, and certain dependent family members may qualify for benefits after a worker’s death.

- Disability Benefits (SSDI)Available to qualifying workers who become unable to work due to a disabling medical condition.

- Supplemental Security Income (SSI)A needs-based program that helps older adults and individuals with disabilities who have limited income and resources.

- Dependent BenefitsCertain children and dependents may qualify for benefits based on a parent’s Social Security record.

Understanding which category applies to your family is the first step toward maximizing available support.

What Social Security Benefits Actually Pay in 2026

One of the most common questions families ask is how much they can expect to receive.

While benefit amounts vary widely based on earnings history and claiming age, these estimates provide a useful starting point.

Average Monthly Benefits in 2026

| Benefit Type | Estimated Monthly Benefit |

|---|---|

| Retired Worker | $2,050–$2,300 |

| Retired Couple | $3,300–$4,000 |

| Disabled Worker (SSDI) | $1,600–$2,000 |

| Survivor Benefit | $1,700–$2,300 |

| SSI Individual | Up to approximately $980 |

Factors That Affect Your Benefit Amount

Your monthly payment depends on:

- Lifetime earnings history

- Number of working years

- Claiming age

- Marital status

- Survivor eligibility

- Cost-of-living adjustments (COLA)

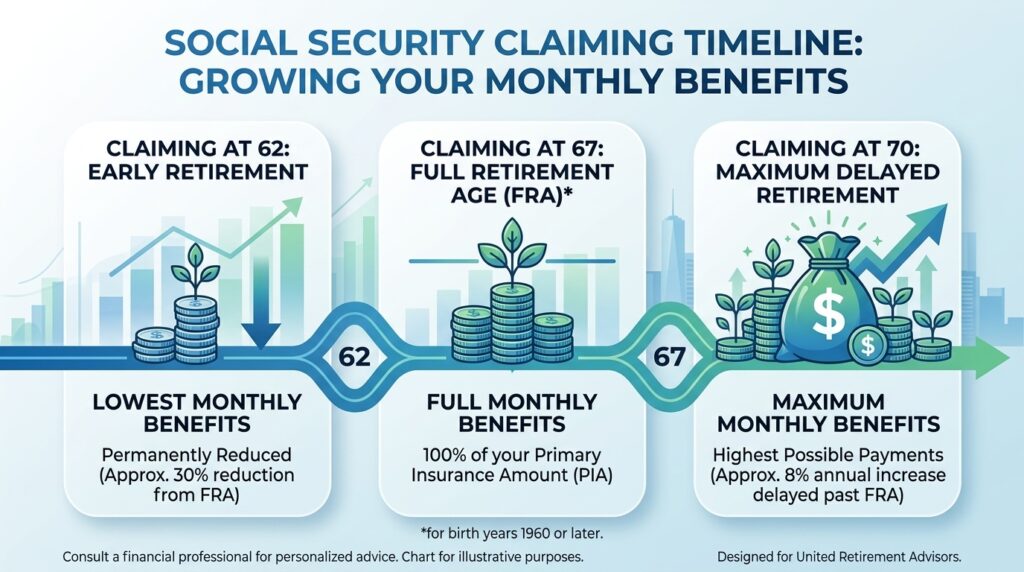

The Impact of Claiming Age

Claiming age can dramatically affect monthly income.

- Age 62: Reduced benefit

- Full Retirement Age (67 for most current retirees): Standard benefit

- Age 70: Maximum delayed retirement credits

Someone eligible for $2,500 at full retirement age may receive closer to $1,750 by claiming early at 62, while delaying until age 70 could increase benefits to more than $3,000 per month.

[💡 Tip]

Delaying Social Security benefits until age 70 may significantly increase guaranteed lifetime income. For healthy retirees with other income sources, waiting can be one of the most effective retirement planning strategies available.

Regional Cost Differences Matter

Although Social Security benefits are generally the same nationwide, purchasing power varies dramatically.

A monthly benefit that comfortably supports retirement expenses in rural communities may cover only a portion of housing costs in high-cost areas such as California, New York, Massachusetts, or Hawaii.

This makes location an important part of retirement planning.

How to Pay for It / Financial Options

Unlike healthcare or senior care services, Social Security itself is a source of income rather than an expense. However, families often need to understand how it works alongside other financial resources.

Social Security as a Retirement Foundation

Many retirees combine Social Security with:

- Employer pensions

- 401(k) withdrawals

- IRA distributions

- Personal savings

- Investment income

Medicare and Social Security

Many beneficiaries enroll in Medicare when they become eligible.

Medicare may cover:

- Hospital insurance (Part A)

- Medical insurance (Part B)

- Prescription drug coverage (Part D)

However, Medicare premiums may be deducted directly from Social Security payments.

Medicaid Support

For lower-income seniors, Medicaid can help cover:

- Long-term care services

- Nursing home costs

- Certain medical expenses

Social Security income is often considered when determining eligibility.

Veterans Benefits

Eligible veterans may receive additional income and healthcare assistance through federal veterans programs.

These benefits can complement Social Security and reduce out-of-pocket expenses.

Tax Considerations

Some retirees are surprised to learn that Social Security benefits may be taxable depending on total household income.

Consulting a qualified tax professional can help reduce unexpected tax liabilities.

How to Decide When to Claim Benefits

Choosing when to start Social Security is one of the most important retirement decisions you’ll make.

Step 1: Estimate Your Monthly Benefit

Review your earnings record and projected benefit amount.

Verify:

- Employment history

- Reported earnings

- Estimated retirement age benefits

Step 2: Evaluate Your Health

Consider:

- Life expectancy

- Family medical history

- Current health conditions

Longer life expectancy often makes delaying benefits more attractive.

Step 3: Assess Other Income Sources

Ask yourself:

- Do you have retirement savings?

- Will you continue working?

- Can you cover expenses while delaying benefits?

Step 4: Consider Your Spouse

Married couples should coordinate claiming strategies carefully.

The timing of one spouse’s claim can affect:

- Spousal benefits

- Survivor benefits

- Lifetime household income

Step 5: Meet With a Financial Professional

A retirement income analysis can help determine the claiming strategy that best fits your family’s goals.

Signs It’s Time to Review Your Social Security Strategy

Many people claim benefits without fully understanding their options.

Consider reviewing your strategy if any of the following apply:

- You’re approaching age 62

- You’re within five years of retirement

- You’re recently widowed

- You’re divorced after a long-term marriage

- You’re considering working during retirement

- You have concerns about retirement income

- You’re caring for aging parents

- Your health situation has changed

- You’re planning to relocate

- You have questions about Medicare enrollment

- You’re unsure about survivor benefits

A proactive review can prevent costly mistakes that may affect income for decades.

Frequently Asked Questions

Can I collect Social Security and continue working?

Yes. However, if you claim benefits before reaching full retirement age and continue working, your benefits may be temporarily reduced if earnings exceed annual limits. Once full retirement age is reached, those limits generally no longer apply.

Will Social Security cover all my retirement expenses?

For most retirees, Social Security replaces only a portion of pre-retirement income. Additional savings, investments, pensions, or other income sources are typically needed to maintain a comfortable lifestyle.

Can divorced spouses receive Social Security benefits?

Yes. In many cases, individuals who were married for at least 10 years and remain unmarried may qualify for benefits based on a former spouse’s earnings record, even if that former spouse has remarried.

Final Thoughts

A Social Security Benefit is far more than a monthly check—it’s a critical piece of retirement security for millions of American families. Understanding benefit types, payment amounts, claiming strategies, tax implications, and coordination with Medicare or other income sources can help you make informed decisions that strengthen long-term financial stability.

The earlier you begin planning, the more options you’ll have. Whether retirement is around the corner or years away, taking time to understand your Social Security choices today can lead to greater confidence and financial peace of mind tomorrow.